Cocoa Will Dip, Then Pop

July 31, 2023 by admin

Filed under Commodities News

Short-term, cocoa prices will be tepid, but longer term, they will heat up, given growing global demand for quality chocolates.

Cocoa Will Dip, Then Pop

July 31, 2023 by admin

Filed under Commodities News

Short-term, cocoa prices will be tepid, but longer term, they will heat up, given growing global demand for quality chocolates.

UK Gov’t Department of Energy and Climate Change Pathways 2050 report - July 30

July 31, 2023 by admin

Filed under Natural Gas

-2050 Pathways Analysis

-UK energy scenarios: working with a flawed model

-DECC publishes plans for achieving 2050 targets

-DECC lays out six possible futures for low-carbon energy

read more

How long will the Chinese put up with coal?

July 31, 2023 by admin

Filed under Natural Gas

Exxon Mobil today issued an impressive second-quarter earnings report, with much of the good news again involving a surge in liquid natural gas production from Qatar. It’s further proof that Exxon — along with the rest of Big Oil — has made a big bet that natural gas will be a growth engine for the company in the absence of opportunities in oil. Fast-growing Asia is the big market, with China leading the way.

read more

UK Gov’t Department of Energy and Climate Change Pathways 2050 report - July 30

-2050 Pathways Analysis

-UK energy scenarios: working with a flawed model

-DECC publishes plans for achieving 2050 targets

-DECC lays out six possible futures for low-carbon energy

read more

ODAC Newsletter - July 30

![]() Another week on and there has been no further leak from the BP Macondo well. Officials are now “optimistic” about preparations for a new attempt at a, with the initial step of pumping mud into the top of the well likely to begin as soon as Sunday. With the leak apparently under control, BP chose this week to announce the inevitable departure of its CEO Tony Hayward, whose replacement by the American Bob Dudley was vital for the company’s damage limitation efforts in the US…

Another week on and there has been no further leak from the BP Macondo well. Officials are now “optimistic” about preparations for a new attempt at a, with the initial step of pumping mud into the top of the well likely to begin as soon as Sunday. With the leak apparently under control, BP chose this week to announce the inevitable departure of its CEO Tony Hayward, whose replacement by the American Bob Dudley was vital for the company’s damage limitation efforts in the US…

read more

Peak Moment 175: Time’s up! an uncivilized solution (with transcript)

What kind of life do you want, and what are you willing to do to get it? Keith Farnish, author of Time’s Up! An Uncivilized Solution to a Global Crisis, sees industrial civilization as the most destructive way of living yet devised by humans. And it’s over: environmental degradation and depletion tell us it can’t continue. The system has myriad ways to make us believe we can’t live without it. But Keith believes we can - there are countless ways to move forward into contented, happy, and full lives. We can “disengage” and reconnect with the natural world, ourselves, and others.

What kind of life do you want, and what are you willing to do to get it? Keith Farnish, author of Time’s Up! An Uncivilized Solution to a Global Crisis, sees industrial civilization as the most destructive way of living yet devised by humans. And it’s over: environmental degradation and depletion tell us it can’t continue. The system has myriad ways to make us believe we can’t live without it. But Keith believes we can - there are countless ways to move forward into contented, happy, and full lives. We can “disengage” and reconnect with the natural world, ourselves, and others.

read more

How long will the Chinese put up with coal?

Exxon Mobil today issued an impressive second-quarter earnings report, with much of the good news again involving a surge in liquid natural gas production from Qatar. It’s further proof that Exxon — along with the rest of Big Oil — has made a big bet that natural gas will be a growth engine for the company in the absence of opportunities in oil. Fast-growing Asia is the big market, with China leading the way.

read more

BP’s Deepwater Horizon - Static Top Kill vs. Bottom Kill: Weighing the Risks - and Open Thread

Author’s Note: Art Berman (aeberman) is an Oil Drum staff member and geological consultant whose specialties are subsurface petroleum geology, seismic interpretation, and database design and management. He has been interviewed on CNN and BNN about the Deepwater Horizon disaster. William Semple collaborated on this post. Mr. Semple is a drilling engineer and independent drilling consultant with 37 years of experience in the oil and gas industry. He worked for 16 years with a major oil company and has 24 years of experience as a drilling supervisor. He has been a guest contributor on The Oil Drum writing about the Deepwater Horizon (June 19, 2023).

A permanent solution to the BP Macondo blowout in the Gulf of Mexico may be achieved soon but there are risks. Admiral Thad Allen announced on Monday, July 26 that a static top kill would be attempted on August 2. The schedule may be accelerated to July 31 or August 1 according to an announcement today (July 29). The sealing cap has successfully stopped the flow of oil and gas from the well and the pressure continues to build slowly. Temperature at the wellhead has not increased, and seeps near the well are mostly nitrogen and biogenic methane unrelated to leakage. BP Senior Vice President Kent Wells’ technical update on July 21 explained these findings and showed how the well will be killed.

There are risks involved in both the top and bottom kill procedures. The purpose of this post is to describe those risks. There are two risks associated with the static top kill. First, it may not work at all and second, it may rupture the casing by pumping heavy mud under pressure (“bull heading”).

Kent Wells described the static top kill as a process of continuously pumping mud into the well until the oil is pushed into the reservoir. This is clearly erroneous and must be a simplification designed for the general public. What will more probably take place is a practice called “bleed and lubricate”. Heavy mud is pumped into the well through the choke and kill lines on the blowout preventer (BOP) and allowed to sink to the bottom of the well. Hopefully, the mud will retard the flow so that some of the pressure can be bled off by producing oil to the surface for a short period. Then, more heavy mud will be pumped into the well, and the process repeated as necessary until the well contains enough mud to kill the well.

The first problem with stopping the flow from the top is that it has to be an annular kill: the flow was coming up the annulus outside the production casing. This is a very narrow space so mud will have to pumped at high pressure to achieve entry. It will initially be working against a full column of gas and oil and the shut-in pressure at the well head. On the positive side, if produced sand has accumulated in the annulus, the operation may not have to contend with the full force of the reservoir pressure in addition to these obstacles. On the negative side, the well head seals might prevent or restrict downward flow, or the pumping pressure could rupture the 22-inch casing, or reach a pressure high enough to call off the operation.

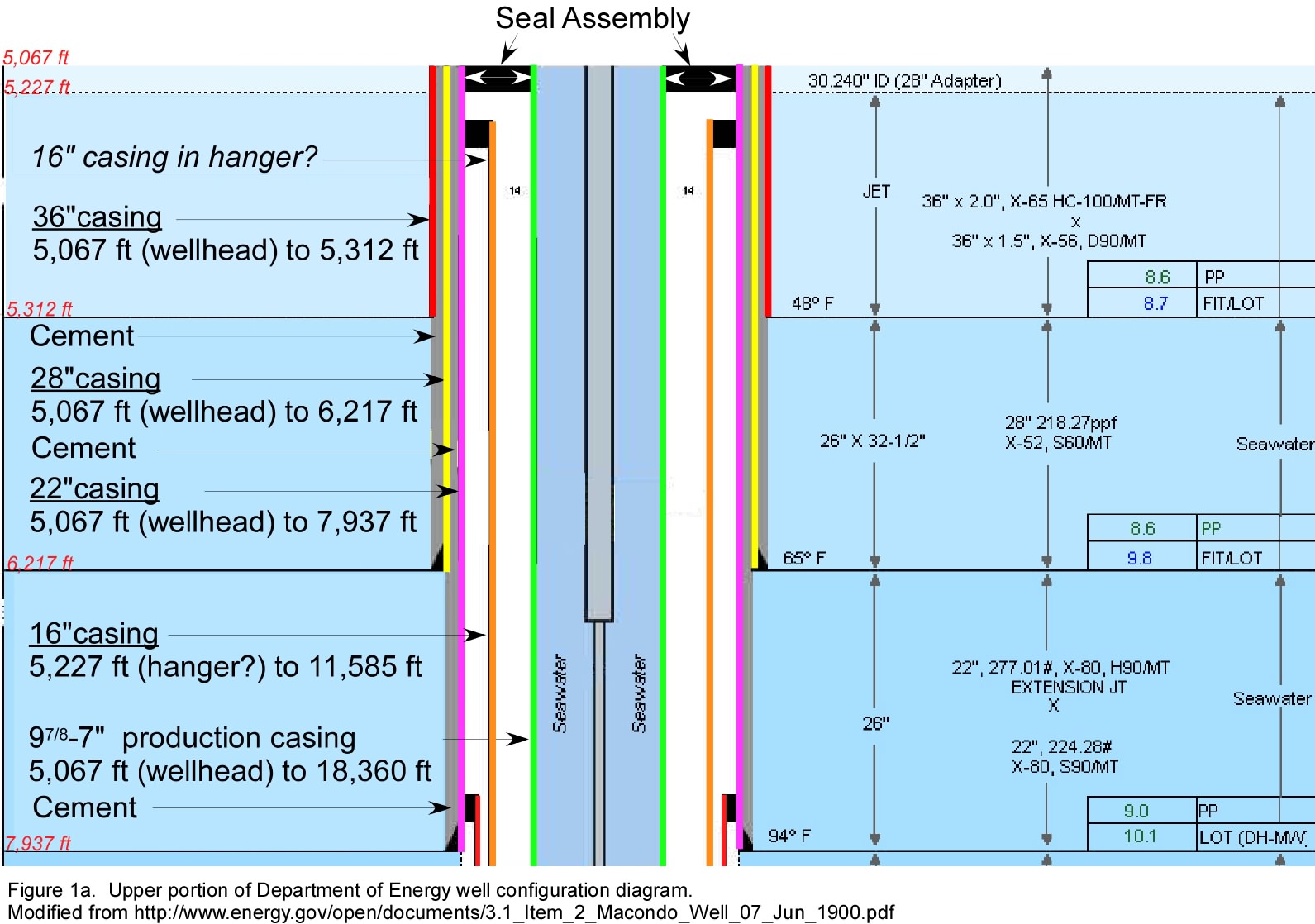

Figure 1a (based on a government document) shows that the upper part of the well bore is protected by three strings of casing (36-, 28-, and 22-inch) and cement down to 7,937 feet (measured depth below sea level). A fourth string of 16-inch casing extends nearly from the well head to where it is cemented at 11,585 feet, but it is apparently hung inside the 22-inch casing at 5,227 feet, leaving a gap of 160 feet. The 16-inch pipe has a burst rating approximately equal to the current shut-in pressure of 6,900 psi (80% of rating), but the 22-inch pipe does not meet this standard.

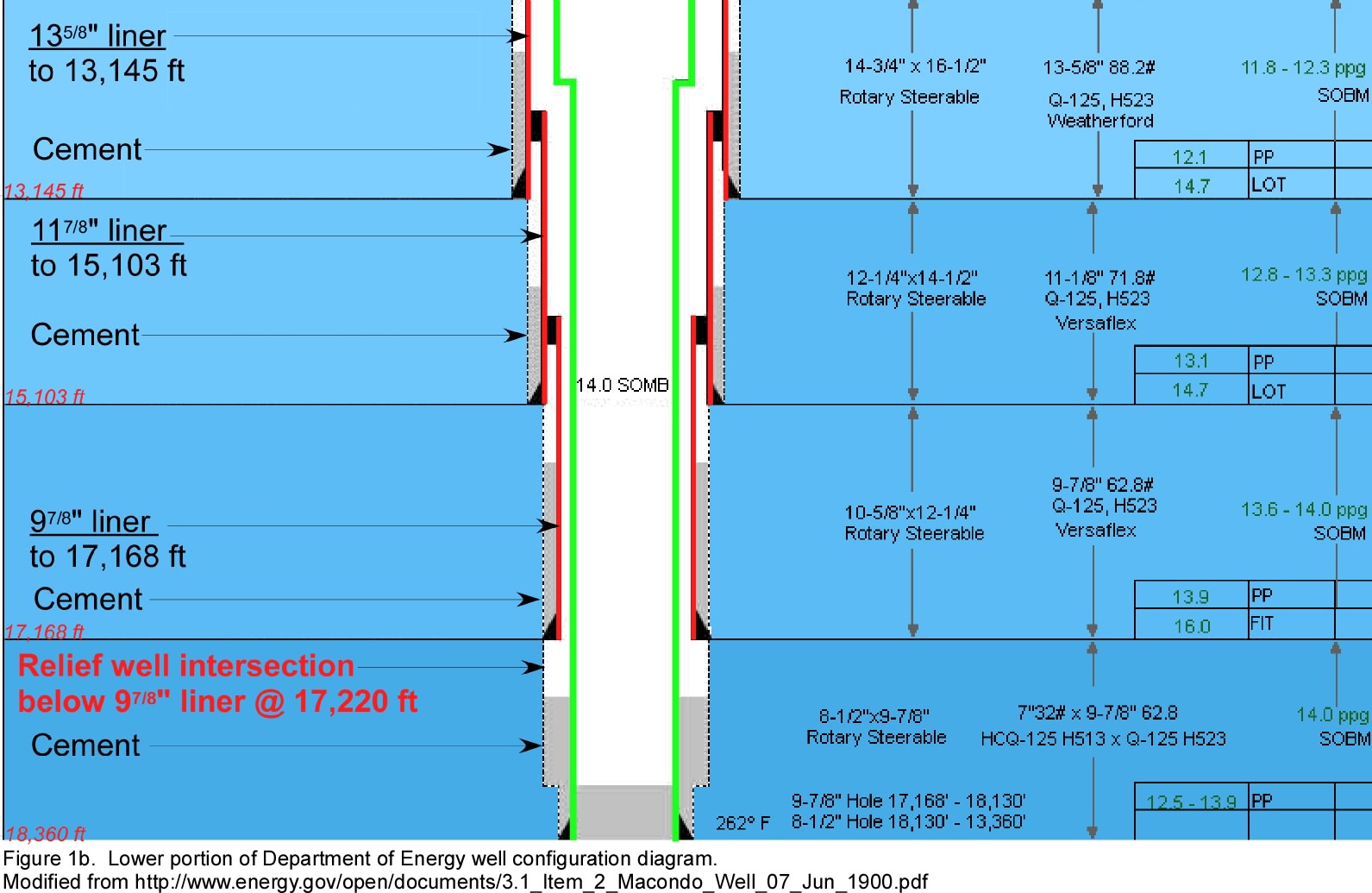

BP has said that the relief well DD3 plan will continue regardless of the success of the top kill operation. The main risk with a bottom kill is that it may take considerable time to accomplish. Because of the recent tropical storm, crews are just removing the storm packer today, and it will take time to re-enter and condition the hole before drilling resumes. BP estimate that the DD3 will intersect the Macondo well around August 10. Most efforts to intersect a blown-out wells require several attempts. The recent 2009 Montara blowout in the Timor Sea required four attempts that took a month after the relief well was near the blow out and cased. The bottom of the first Macondo relief well is currently located a few feet from the target at approximately 17,220 feet measured depth (based on Wells’ update and shown in Figure 1b).

The good news is that, in this case, the relief well does not, apparently, need to intersect the well exactly-it just needs to be close. Once the relief well penetrates the reservoir, enough mud can be pumped to hopefully overcome flowing pressure and kill the well. The bottom-kill option has the same annular flow path liabilities as the top kill, but it has the capacity to deliver higher flow rates directly to the reservoir. This approach will not cause significant pressuring near the well head and should not, therefore, pose a risk of rupturing the 22-inch casing.

The bottom kill option involves considerably less mechanical risk than the top kill, but time is the enemy, so the top kill makes sense. Maintaining the objectivity to abandon the operation rather than risk casing rupture will be critical.

Hollow Men of Economics

This is a guest post by Gregor MacDonald. Gregor is an oil analyst and energy sector investor, who, in his words, “also focuses on the coming transition to alternatives”. This post was previously published on Gregor.us.

Left unaddressed during the past 3 years in most of the debates between economists has been the problem of energy. The reason is simple: post-war economists don’t do energy, except as an ever-expanding resource that the credit system and technology makes available. For the post-war economist, the supply curve of energy-save for brief lags-is always coming back into rough equilibrium with the economy.

Accordingly, the ongoing dispute between Keynesians and Austrians (or Austerians if you like) is exceedingly boring in this regard. As late as 2008, for example, economist Paul Krugman was at least an infrastructure-and-engineering Keynesian. However, Paul quickly converted to becoming just a throw lots of money at the existing system Keynesian. The hollow nature of Krugman’s debate with Niall Ferguson meanwhile comes via their shared belief that the system will self-organize, if you follow their respective prescriptions. They are indeed the inheritors of Adam Smith.

However, neither allowing the economy to deflate further from here via austerity, nor throwing more debt-marked stimulus will solve the present day problem. For the United States, along with the rest of the developed world, has reached a boundary in energy.

Only an economist could wonder in their leisure now, whether energy played a significant role in our current crisis. Indeed the public remarks of Ben Bernanke on the matter of energy, during the 2005-2010 period, were at least as clueless as his embarrassing commentary on the historic bubble in housing and credit. As the nation’s chief economist, Bernanke saw no problem with credit, with derivatives, with the fast inflation in housing prices, or with energy prices. And as an American economist, he was not alone.

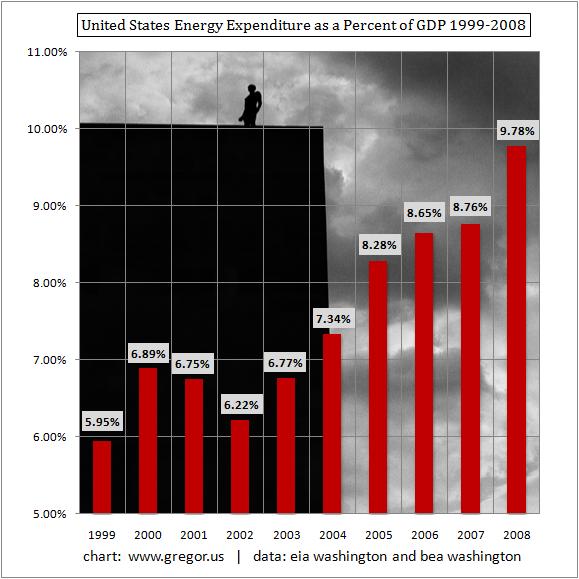

As state’s see their budgets collapse and start a new round of layoffs, we should consider the fact that house price inflation masked the lack of wage growth in the United States. And now that house prices continue their descent for a 5th year, American workers are more fully exposed to the decade-long march higher in energy costs. They can experience this individually through energy prices, or more generally through the overall energy cost to the economy. Hence, the chart above.

Unlike many who were either shocked or angered at the ridiculous paper released by Richmond Fed Economist Kartik Athreya, Economics is Hard, I was delighted. For, the paper confirms that at the Federal Reserve, just as in the post-war economics profession, competency has been replaced with authority. Indeed, this was in fact Athreya’s central point: that only a PhD in economics conferred the proper access to discuss economic issues. The most beautiful rebuttal came from Ambrose Evans-Pritchard, who made a point dear to me and one that I have made for years: economics is a social science, not a science. In other words, economists are working down here, alongside the rest of us humanists. History, literature, psychology, and anthropology to mention a few disciplines are all equally competitive fields of knowledge to understand the system of behavior known as an economy. Accordingly, it behooves post-war economists to dislodge themselves of the view that their discipline neatly explains energy and energy supply. Lose the attitude. The problem of energy limits awaits you.

-Gregor

Chart: United States Energy Expenditure as a Percent of GDP 1999-2008. Data used is the latest available. GDP series comes from the US Department of Commerce, Bureau of Economic Analysis. Energy Expenditure data comes via EIA Washington’s SEDS series, for all states and also the country as a whole. I put these two data series together on my own, but, checked it against EIA Washington’s own calculation of Total Energy Expenditures vs GDP. 2009 is not omitted from the chart by choice, but rather, because expenditure data is not easily available yet for that year. Background photo is of a rooftop sculpture by Antony Gormley from his project Event Horizon, which was displayed in both London and New York.