ODAC Newsletter - Oct 30

October 31, 2022 by admin

Filed under Natural Gas

![]() Oil prices vacillated this week, falling back from their recent high on news of unexpectedly large US inventories, later rallying as the US economy officially emerged from recession…

Oil prices vacillated this week, falling back from their recent high on news of unexpectedly large US inventories, later rallying as the US economy officially emerged from recession…

read more

Critique of Scientific American’s October, 09 essay: Squeezing More Oil from the Ground

October 31, 2022 by admin

Filed under Natural Gas

Critique of October, 2009 issue of Scientific American essay: Squeezing More Oil from the Ground

read more

Critique of Scientific American’s October, 09 essay: Squeezing More Oil from the Ground

Critique of October, 2009 issue of Scientific American essay: Squeezing More Oil from the Ground

read more

The Future of European Transport: iTREN-2030

On 21 October the final workshop was held in Brussels (Belgium) of the integrated transport and energy baseline until 2030 (iTREN-2030) modeling project. At the workshop a final scenario was presented that incorporated likely transport and energy policies, and the effects on European transport of a continued global plateau in oil production up to 2030. The integrated scenario was generated by four energy and transport models that have been linked in iTREN-2030 to increase the forecasting power of the transport policies of the European Commission.

read more

The recession is dead … long live the recession!

The world’s first peak-oil recession has come to a close, according to third-quarter numbers invented by the federal government. Apparently dumping trillions of dollars onto big banks, insurance companies, and automobile manufacturers interrupted the plummeting descent of American Empire. The stock markets skyrocketed expectedly. Predictably, so did the commodities markets.

read more

ODAC Newsletter - Oct 30

![]() Oil prices vacillated this week, falling back from their recent high on news of unexpectedly large US inventories, later rallying as the US economy officially emerged from recession…

Oil prices vacillated this week, falling back from their recent high on news of unexpectedly large US inventories, later rallying as the US economy officially emerged from recession…

read more

Critique of Scientific American’s October, 09 essay: Squeezing More Oil from the Ground

Critique of October, 2009 issue of Scientific American essay: Squeezing More Oil from the Ground

read more

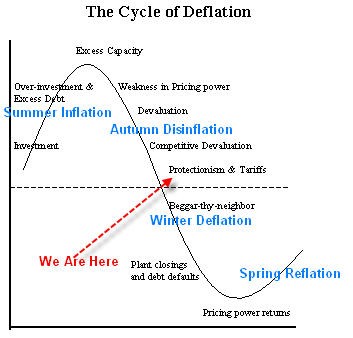

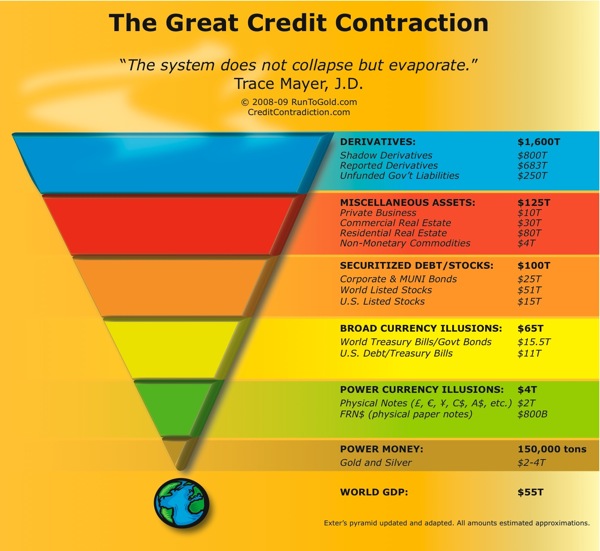

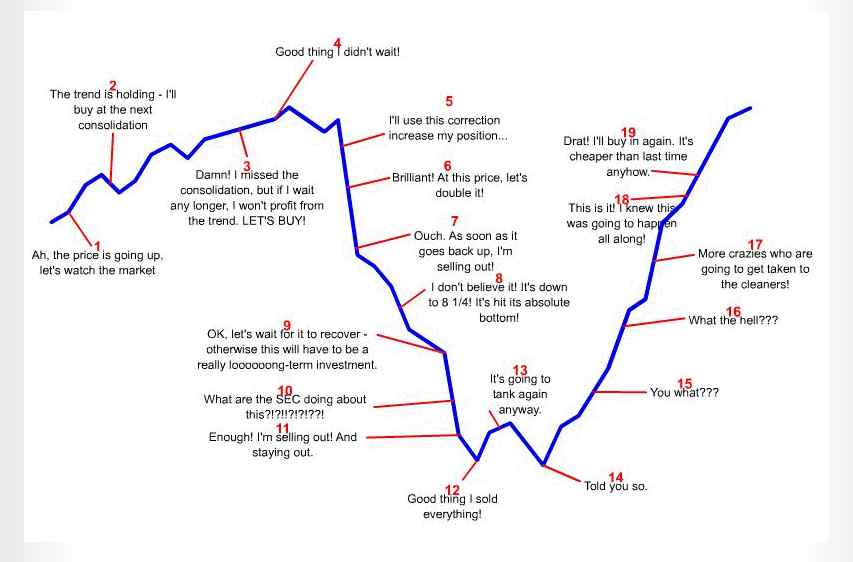

An interview with Stoneleigh - the case for deflation

At the ASPO conference in Denver, October 2009, I had the good fortune to meet Stoneleigh, former editor of The Oil Drum Canada, who left the The Oil Drum crew with colleague Ilargi to set up The Automatic Earth where they publish stories, news and analysis of the unfolding financial crisis. I spent a couple of days chatting with Stoneleigh where she recounted her rather gloomy prospects for the immediate future of the global economy. The following interview is a summary of her analysis of the unfolding situation. Note that in a departure from convention, my questions are set in “blockquotes” to distinguish these from Stoneleigh’s responses.

Stoneleigh, the world economy seems to be suffering from two great structural woes at present, namely stubbornly high energy prices that are linked to demand that is persistently ahead of the supply curve, and a level of debt that has destabilized the global finance and banking systems. Can you explain for us the scale and structure of this debt and to what extent write-downs and quantitative easing (QE) have solved this problem?

Firstly, I would say that the energy prices that currently seem stubbornly high should fall substantially as the speculative premium evaporates and demand falls on a resumption of the credit crunch. The sucker rally that has spawned all the talk of green shoots is essentially over in my opinion. The result should be a reversal of a number of trends that depend on the ebb and flow of liquidity - we should see stock markets and commodity prices fall, a significant resurgence in the US dollar and a large contraction of credit. The scale of the reversal should be substantial, as should its effects on energy demand. Demand is not what one wants, but what one is ready, willing and able to pay for, and in a severe credit crunch the capacity to pay for supplies of most things will be severely reduced.

Figure 1

As demand falls, and with it prices, investment in the energy sector is likely to dry up. Many projects will be uneconomic at much lower prices, meaning that the projects which might have cushioned the downslope of Hubbert’s curve (and the much steeper net energy curve), are unlikely to be developed. In this way a demand collapse sets the stage for a supply collapse that could place a hard ceiling on any prospect of economic recovery. That is a recipe for extremely high energy prices in the future.

Secondly, our vulnerability to the consequences of debt is extremely high at the moment. The scale of that debt is staggeringly large. The global credit hyper-expansion has been decades in the making and is now significantly larger than notable events of the past such as the South Sea Bubble of the 1720s and the Tulip Bubble of the 1630s. It dwarfs the excesses that led to the Great Depression.

Figure 2

Credit bubbles are inherently self-limiting, proceeding until the debt they generate can no longer be supported. We have already passed that point, and we are now two years into a contraction phase that is about to accelerate. As the aftermath of a credit bubble is typically proportional to the scale of the excesses that preceded it, we should be in for the largest economic contraction in at least several hundred years, and it will be global.

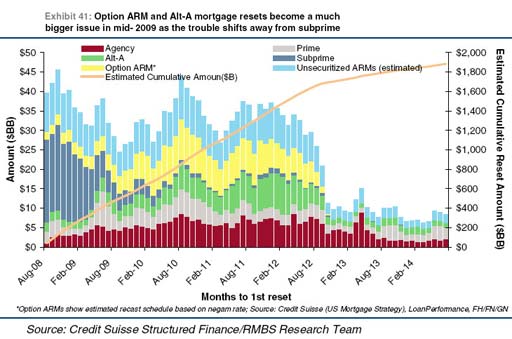

Real estate, which is a major focus of the mania, should do particularly badly in the coming years (in fact the coming decades or longer). There is still so much deleveraging ahead, and so many danger signals, such as the scale of the coming interest resets on US mortgages between now and 2012 (below). While the subprime resets are ending, Alt A and Option ARMs are just beginning.

Figure 3

There will be a very significant undershoot of historically average values, as there always is following a mania (much more than the Case-Shiller projection below suggests). In my opinion, housing prices are likely to fall at least 90% on average. For those who own property on margin, this will be a disaster.

Figure 4

For evidence that this crisis is indeed global, look, for instance, at European housing bubbles, which were worse than in the US.

Figure 5

Figure 6

Unlike inflation, which divides the underlying real wealth pie into smaller and smaller pieces, credit expansion creates multiple and mutually exclusive claims to the same pieces of pie. Once a credit expansion reaches its maximum extent, and contraction begins, these excess claims begin to be extinguished. Unfortunately, the leverage is such that there are probably over a hundred claims to each piece of pie. While contraction begins slowly, as is the nature of positive feedback loops, it picks up momentum until a cascade point is reached, whereupon one can expect the excess claims to be extinguished in a rapid and chaotic process. This amounts to a rapid collapse in the supply of money and credit relative to available goods and services, which is the definition of deflation.

Figure 7

The scale of the problem has been temporarily concealed by a market rally and the shovelling of tens of trillions of dollars of taxpayer’s money into a giant black hole of credit destruction. This has done nothing to reignite lending, but the temporary (and entirely irrational) resurgence of confidence has restored a measure of liquidity. As that confidence evaporates with the end of the rally, that liquidity will also disappear

Banks hold extremely large amounts of illiquid ‘assets’ which are currently marked-to-make-believe. So long as large-scale price discovery events can be avoided, this fiction can continue. Unfortunately, a large-scale loss of confidence is exactly the kind of circumstance that is likely to result in a fire-sale of distressed assets. The structure of the credit default swap component of the derivatives market makes this very much more likely.

The CDS market allowed large bets to be placed on certain prices falling, and by entities which did not have to own those assets. This creates a perverse incentive for some parties to cause others to fail for profit (akin to me being able to take out fire insurance on your house and thereby give me an incentive to burn it down). An added complication is the extreme degree of counterparty risk that resulted from a complete lack of capital adequacy regulation. Many parties with winning bets will not be able to collect, so they may cause financial mayhem for nothing. The CDS market is worth some $62 trillion, and a meltdown is very likely in my opinion.

A large-scale mark-to-market event of banks illiquid ‘assets’ would reprice entire asset classes across the board, probably at pennies on the dollar. This would amount to a very rapid destruction of staggering amounts of putative value. This is the essence of deflation.

I have for a long time argued and believed that there are so many interests vested in protecting our current system that national governments, the IMF and institutions working together would keep the market flooded with liquidity in order to ward off the threat of deflation. In fact, it seems that a prolonged period of inflation is the only way to diminish our debts. I sensed at ASPO International in Denver that this was the majority view. Do you agree that inflation is the most likely near term outcome of current monetary policy?

Figure 8

Absolutely not. I agree that this is the consensus opinion, but I see it as fundamentally mistaken. The debt monetization that is going on has done nothing to increase the supply of money and credit relative to available goods and services, which is the definition of inflation. Credit contraction dwarfs debt monetization, leaving us in a state of net contraction, even though we have just experienced a large rally lasting months, which should have been the most favourable condition for reigniting lending if such a thing were in fact possible. I would argue that it is simply not possible and that deflation is inevitable.

Figure 9

Figure 10

Credit bubbles always end this way, with the mass extinguishing of the excess claims debt represents. They are essentially Ponzi schemes, crucially dependent on the continued buy-in of new entrants. Globalized finance brought a flood of new entrants following the liberalization of the early 1980s, but there are now no more new sources of wealth to tap. Deregulation allowed the reckless to gamble away virtually everything, including bank deposits and pension funds. Globalized finance has created a giant Enron, which while appearing robust is actually almost completely hollowed out. Such structures implode, often without much notice.

Figure 11

In my opinion, deflationary deleveraging will continue until the (small amount of) remaining debt is acceptably collateralized to the (few) remaining creditors. Until that point, there can be no lasting return of the confidence required to rebuild shattered credit markets. Deflation is ultimately psychological. Without trust we will see hoarding of the cash which will be very scarce in the absence of the credit that currently comprises the vast majority of the effective money supply. The combination of scarce cash and a very low velocity of money will be toxic.

Money is the lubricant in the economic engine and without enough of it that engine will seize up as it did in the 1930s, when farmers dumped milk they couldn’t sell into ditches while others were starving for want of the money to buy food. There was plenty of everything except money, and without money, one cannot connect buyers and sellers. Potential buyers will have no purchasing power as they will have lost access to credit and their ability to earn an income will be hit by spiking unemployment. Those who still have jobs will find that they have no bargaining power and there is therefore no wage support. Sellers and producers will have no market and will themselves lose the means to purchase supplies or raw materials for the things they would like to produce. If conditions remain frozen for any length of time, they will go out of business. The deeper the collapse, the more protracted the trough and the more difficult the eventual recovery.

Figure 12

I would argue that we have no need to fear inflation until we have reached a trough - until the deleveraging impulse is spent. We can expect to spend a long time in the liquidity trap, where real interest rates will be much higher than nominal rates, leaving central bankers “pushing on a string”.

Some would argue that faced with the unimaginable specter of deflation that governments will seize control of interest rates from the bond market. Why do you think this may not happen?

The bond market is far more powerful than governments at this point. While the international debt financing model remains, the bond market will retain its power to prevent money printing. Even though governments are not succeeding in increasing the effective money supply for reasons already discussed, they are nevertheless increasing systemic risk with their activities. This is a recipe for very much higher interest rates as a risk premium. Governments do not set interest rates, they decide what rate to defend, but if that rate is substantially different from what the bond market requires, then defending it would be ruinous.

Figure 13

I think we are headed (not imminently but eventually) for a bond market dislocation, with nominal interest rates on government debt spiking into the double digits. This will amount to hitting the emergency stop button on the economy, especially since real interest rates will be substantially higher (the nominal rate minus negative inflation). I am in fact expecting interest rates on private debt to rise before we see problems in the market for government debt, as the latter should benefit substantially in the shorter term from a flight to safety. The risk premium on private debt is already rising, which is a serious danger signal for such thoroughly indebted societies as we see in the developed world.

But stock markets are booming again, several OECD economies are emerging from recession, unemployment has stabilized, there are green shoots everywhere. Surely the current QE strategy is working?

The green shoots are gangrenous. Some of the largest market rallies on record happened during the course of the Great Depression, as depressions are associated with very high volatility. Look for instance at the great sucker rally of 1930. There are always rallies of all different sizes in any bear market, just as there are pullbacks of all sizes in bull markets. No market ever moves in only one direction.

People tend to extrapolate recent trends forward, but this amounts to stepping on the gas while looking only in the rearview mirror. This is one reason why major trend changes are so rarely anticipated. Another is that the prevailing view of markets is fundamentally wrong. There is no perfect information, perfect competition, stabilizing negative feedback, rational utility maximization or efficient markets. Markets are irrational, driven by swings of optimism and pessimism, or greed and fear, in an endless tug of war, and largely in an information vacuum. Investors chase momentum by jumping on passing bandwagons, hence demand for financial assets increases when prices are rising and falls when prices are falling, in classic positive feedback loops.

Figure 14

We have just lived through a period of several months when greed and complacency were in the ascendancy, but that trend is about to reverse in my opinion. Looking at markets as constructs of human herding behaviour allows them to be probabilistically predictable, permitting the forecasting of trend changes. For anyone who is interested in pursuing this idea further, I suggest looking into Bob Prechter’s socionomics - a fascinating subject which delves into the many effects of changes in collective mood.

For instance, as pessimism deepens, driving economic contraction, one would expect to see many manifestations of collective anger and mistrust. As this progresses it is likely to lead to xenophobia and a blame-game, with skillful manipulators (such as the fascist BNP leader Nick Griffin in the UK) poised to direct the anger of the herd towards their own chosen targets. The potential for serious social fragmentation is very high when expectations have been dashed and there is not enough to go around. Having lived through a very long period of manic optimism and increasing inclusion, we in the developed world are not used to expressions of the dark side of human nature, except for entertainment purposes in popular television programmes. It will come as a considerable shock.

Would you care to give your opinion on where the Dow Jones Industrial Average is headed in the near (1 year) and medium terms (2 to 5 years)?

I think the market will fall hard (intervening short rallies notwithstanding) for perhaps 18 months. This was the length of the first leg down (October 2007-March 2009) and so represents a reasonable first guess at how long the next leg at the same degree of trend might last. I think we will see falls of thousands of points in a series of cascades. I don’t see the markets reaching a lasting bottom until probably the middle of the next decade, and even then I don’t expect it to be a final bottom. This has been the largest credit bubble in history, and the aftermath of a major bubble always undershoots where it began before any kind of recovery begins.

Figure 15

The aftermath of the last major mania - the South Sea Bubble in the 1720s - lasted decades and culminated in a series of revolutions.

Figure 16

We are still relatively near the beginning of our own crisis, but already it compares with the Great Depression.

How do you see the US$, gold and oil trading in the same time frame?

I think almost all assets will fall as price support is knocked out from underneath them, but the dollar should rise initially on a flight to safety. Scarce cash will be king for a long time, and the value of one’s currency relative to available goods and services domestically will matter much more for most people than its value relative to other currencies internationally.

In a deflationary scenario, prices fall, but purchasing power typically falls even faster, meaning that everything becomes less affordable despite the lower nominal prices. Prices in real terms, adjusted for changes in the supply of money and credit, are what matter. In a world where almost everything is becoming rapidly less affordable, the essentials will be the least affordable of all, as a much larger percentage of a much smaller money supply will be chasing them. This will confer relative price support.

Although we could initially see a large glut in energy supply as demand falls off a cliff, this is likely to lead to supply collapse as investment dries up, hence I expect energy prices to bottom early in this depression. Both financial and physical risks to energy exploration are likely to increase substantially in a destabilized and capital constrained world, and even maintaining existing assets could become very difficult. This is a recipe for much greater state involvement in ownership and exploitation of (probably deteriorating) energy assets, with increasing conflict over those assets as supply gets dramatically tighter with lack of investment.

As for gold, I expect it to fall initially as people sell not what they would like to, but what they can, in order to raise the cash they need for living expenses and debt servicing. Owning gold is likely to become illegal again (as it did in the Great Depression) in my opinion. This wouldn’t necessarily stop you owning it, but would stop you trading it (at least without taking major risks) for other things you might need. Owning gold now therefore only makes sense if one is confident of being able to sit on it for a very long time, as it will hold its value over the long term as it has for thousands of years.

What will be the consequences for unemployment levels and services provided by government?

Figure 17

Unemployment will go through the roof as the prospects for selling most goods and services decline dramatically. In the developed world we are nations of middle men - generally service economies where we make a living figuratively taking in each other’s laundry. Most of us produce relatively little. Even those who do will find almost no market for their exports, and those who could find buyers may not be able to send shipments as credit contraction prevents shippers from getting the letters of credit they need to ship goods. A glance at what has happened to the Baltic Dry Index (below) indicates the difficulties already facing shipping companies.

Figure 18

Unfortunately middlemen are almost completely expendable, and the services of others are likely to become unaffordable for the majority very quickly. While there will be a huge surplus of labour, and the few who retain purchasing power will be able to hire anyone they want for very little, most people will have to do everything for themselves, as poor people have done throughout history and as most of the population of the world does now. Not only will we lose access to the paid labour of others, but we will lose our virtual energy slaves as well. This will represent an enormous fall in the standard of living for the vast majority.

Figure 19

Whereas inflation can conceal a fall in purchasing power, so that people may not even realize it is happening, deflation brutally exposes it. Wages would have to fall just to keep purchasing power the same, but keeping it the same will not be an option for cash-strapped employers. In addition, with a large surplus of labour, workers will have no bargaining power. This is a recipe for exploitation the likes of which we have not seen for a very long time, but in the intervening adjustment period it is likely to lead first to war in the labour markets.

I would expect general strikes and a breakdown in the reliability of centralized services such as healthcare, education, power systems, water treatment, garbage (and snow) removal etc. This will be exacerbated by plunging tax revenues for all levels of government, which governments will try to compensate for by raising taxes, on anyone still capable of paying, to punitive levels. We would thus expect rapidly deteriorating services at much higher cost.

Figure 20

Figure 21 (click image to see larger version)

Many people are at risk of being eventually priced out of the market for goods and services, and particularly the essential ones, entirely. In my opinion, we stand on the brink of truly tragic circumstances.

Figure 22

Figure 23

End note:

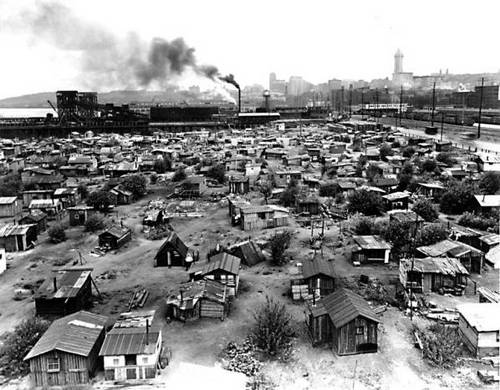

The day before the ASPO conference began in Denver, Stoneleigh, Rembrandt Koppelaar and myself took a drive into the Rocky Mountains National Park providing the opportunity to discuss and reflect upon the current global situation. As the week unfolded I realised that I was in denial about the gravity of the global financial situation. In what has become a situation of complexity that is beyond the ken of most folks, I find it simpler to break this down into smaller components that I can relate to.

In the UK, we have an escalating burden of government debt that we can unlikely ever repay. Unemployment is rising, tax receipts are plunging whilst expenditure on social security, health and the elderly go through the roof. We have been living way beyond our means, which with the peaking of UK oil and gas have suddenly become more meagre. We have an election in May 2010. The new government will want to raise taxes and cut public spending. The current reversal in global growth is sending energy prices higher. Higher unemployment, higher taxes, higher energy prices and reduced public services are a toxic mixture for an ailing economy. If the bond market decides to price in the risk premium for escalating debt it will be game over. The questions are if and when? Figure 13 is one of the more interesting for me.

That’s me on the left and Rembrandt Koppelaar on the right, contemplating our future after a most enlightening, if not very cold day in the Rocky Mountains. Photographer - Stoneleigh.

![]()

The Future of European Transport: iTREN-2030

![]() On 21 October the final workshop was held in Brussels (Belgium) of the integrated transport and energy baseline until 2030 (iTREN-2030) modeling project. At the workshop a final scenario was presented that incorporated likely transport and energy policies, and the effects on European transport of a continued global plateau in oil production up to 2030. The integrated scenario was generated by four energy and transport models that have been linked in iTREN-2030 to increase the forecasting power of the transport policies of the European Commission.

On 21 October the final workshop was held in Brussels (Belgium) of the integrated transport and energy baseline until 2030 (iTREN-2030) modeling project. At the workshop a final scenario was presented that incorporated likely transport and energy policies, and the effects on European transport of a continued global plateau in oil production up to 2030. The integrated scenario was generated by four energy and transport models that have been linked in iTREN-2030 to increase the forecasting power of the transport policies of the European Commission.

In this post I describe the iTREN-2030 project and the different models, covering the POLES global energy supply and demand model in more detail, highlight the conclusions of the present integrated scenario, and give my reflection on the workshop commenting on some areas of improvement to augment the potential of the models.

The iTREN-2030 project is all the more important because the resulting model set and integrated scenario will be used by the European Commission (DG-Tren) in preparing the white paper on transport policies due for 2010. After discussion with the European Parliament and approval by the council of Minister, the European Union will as a result have set out its new course for the future of transport in the period up to 2020.

The iTREN-2030 project

The integrated transport and energy baseline until 2030 (iTREN-2030) project ran for 30 months starting May 2007 and ending October 2009. Funded by the 6th framework program of the European Commission the project aimed to extend the forecasting and assessment capabilities of TRANS-Tools, which is the EU transport network analysis model. Including the potential to include new policy issues. With the end goal of giving the European Commission the possibility to create coherent baselines wherein technology, transport, energy, environment and economic developments until 2030 are integrated. The project was carried out by a consortium of seven institutes among which ISI (Germany), NEA (Netherlands), TRT (Italy), TML (Belgium), IWW (Germany), IPTS (SPAIN), TNO (Netherlands).

In more detail the project entailed linking and improving four different models that already existed, thereby enabling a more integrated modeling exercise on transport and energy. The advantage of linking these models is the creation of a much more detailed outlook. Each model covers its own area (transport network, energy supply, passenger flows, emissions etc.) in much more details than the others do. By linking them many more variables and feedbacks within the system can be taken into account.

The four models are

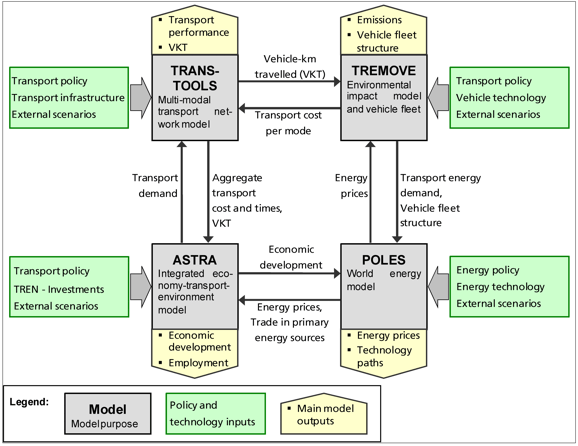

- TRANS-Tools (PDF Description), the model mainly used by the European Commission which gives an overview of the European Transport Network covering passengers and freight and inter modal transport.

- TREMOVE (PDF Description), a model that assesses the effects of different transport and environmental policies on the emissions of the transport sector in EU-27.

- POLES, (PDF Description), a model that simulates long term energy supply and demand developments for different regions of the entire world including sources such as fossil fuels and renewable energy soures as well as energy types such as heat and liquid fuels.

- ASTRA, (PDF Description), a system dynamics model that incorporates technology, employment and energy policy to analyse long-term consequences of European transport policies within the EU-27 plus Norway and Switzerland.

An overview of the four models and how they were linked is given in figure 1 below.

Figure 1 - Overview of the linkages in the iTREN-2030 project between TRANS-Tools, TREMOVE, POOLS and ASTRA, Source: iTREN-2030 website

Limits to understanding: transparency and accessibility of the models

To understand a scenario we need information on which assumptions, formulas and data have been used in its derivation. In the best case detailed documentation is made available alongside a copy of the model itself. Although all the models are accessible to the European Commission and the consortium, some of them are proprietary in case of iTREN-2030. TREMOVE and TRANS-tools can be downloaded at no cost on the internet, but ASTRA and POLES are not available. This creates boundaries in comparing the outcome of these models with other studies. As a consequence most questions at the final workshop were related to understanding what the consortium did on many specific input levels such as how a ‘breakthrough’ in electric cars had been implemented in the model.

The need for transparency was also brought up by the consortium as a recommendation by participants of previous workshops, and by participants in the final workshop. Some effort was made by the iTREN-2030 partners to increase input by organizing two additional workshops were participants were given the possibility to recommend input on specific terrains. One of the outcomes of these additional workshops was the addition of economic crisis effects in the integrated scenario presented at the final workshop.

The POLES Energy Model

Since the Oil Drum is a blog about Energy and our future, and the POLES model covers the energy aspects of this modeling project, I highlight its core as far as information is available. POLES was developed by the French research institute IIEPE-EPE together with French energy consultancy Enerdata and the Institute for Prospective Technological Studies of the European Commission (IPTS). It has seen several iterations and was used in the World Energy Technology 2050 outlook by the European Commission and the 2007 World Energy Council Policy Scenarios (PDF).

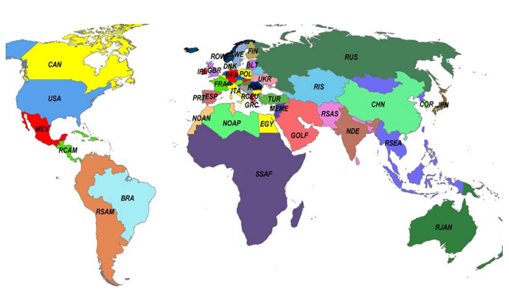

The Poles model divides the world in 47 zones. A total of 32 of these zones represent individual countries including the G7 countries, the European Union countries and BRIC countries. The other countries are modeled as 18 homogeneous regions. For example all of Africa except the northern countries are modeled as the region SSAF

Figure 2 - POLES country and region coverage, Source: iTREN-2030 POLES documentation

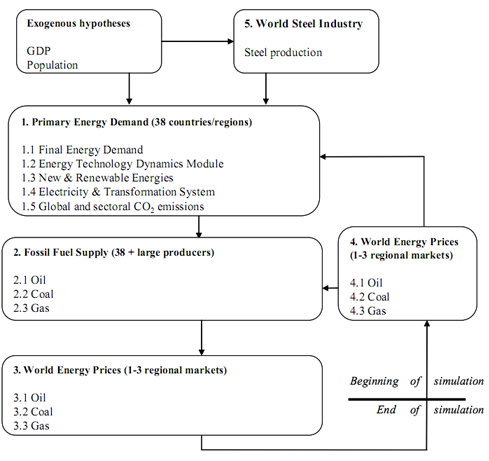

The model employs a ‘backward’ calculation from final energy demand to primary energy supply. Starting with estimating final energy demand in different sectors including different Industries (Steel, Chemical, Non-Metallic, other), Transport Modes (Road, Rail, Air, Other), and RAS (Residential, Service, Agriculture). Separate calculations are made for 12 non-fossil energy technologies and 12 power generation technologies. In the next step diffusion of new & renewable energy technologies is modeled and generation of these sources subtracted from final energy demand resulting in ‘net final energy demand’, subsequently electricity transformation in fossil fuel power plants is ‘undone’ resulting in the needed primary fossil fuels to supply the remaining total fossil) energy demand. Imports and exports are incorporated to simulate trade flows of fossil fuels.

Figure 3 - POLES model overview with arrows indicating model hierarchy, Source: iTREN-2030 POLES documentation

Oil and gas production is simulated by a discovery and reserve modeled using United States Geological Service (USGS) data from the World Petroleum Assessment 2000. Specifically:

- First the model estimates the cumulative amount of oil discovered as a function of the Ultimate Recoverable Resources (revision of USGS numbers with discoveries and production). Incorporating a recovery ratio that increases over time also depending on the price of the resource. In the World Energy Technology Outlook 2050 upon which iTREN-2030 was based the recovery rate for oil increased from 35% today to 50% in 2050.

- Secondly remaining reserves are calculated as being equal to the difference between cumulative discoveries and cumulative production. Using Rt+1 = Rt + DISt - Pt (where R = reserves, DIS = discoveries, P = production, subscript t = year of account).

- Thirdly, the model calculates production for non-OPEC based on a Reserves-to-Production ratio decreasing over time and the calculated remaining reserves, and for OPEC based on the oil needed to balance the oil market (OPEC total oil production = total oil demand - Non-OPEC total oil production).

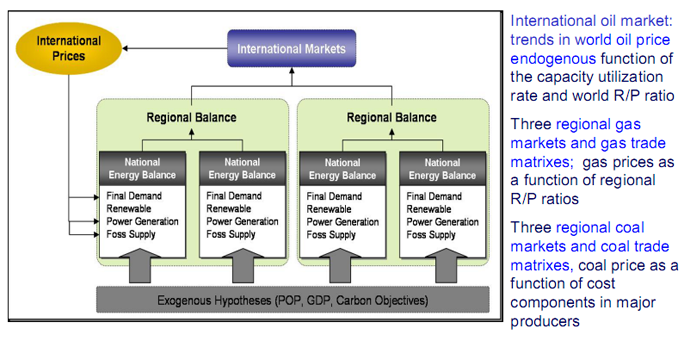

The world oil price in the model is for the short-term based on the rate of capacity utilization in the OPEC gulf, and in the medium and long-term on the world R/P ratio (including unconventional oil). Unconventional oil comes into play at a certain price when it is deemed competitive versus conventional oil. The price of gas is calculated in three different regional markets (US, Europe and ?) depending on demand, domestic production and supply capacity in each individual market. The main driver in gas price determination is the variation in the Reserve-to-Production ratio in each market.

Figure 4 - POLES modeling of international energy market, Source: Enerdata Poles Presentation

More information on the POLES model can be found in this presentation describing the POLES model used for the World Energy Technology 2050 assessment.

An overview of the Integrated Scenario

In the iTREN-2030 an integrated scenario was made to show the effect of linking the various models. It was explicitly mentioned by the consortium that it was not the goal of the project to create the best scenario possible. This was a sub-objective from the main objective of linking and improving the models themselves. Nevertheless it was an interesting scenario worthwhile to show to The Oil Drum readers. The approach taken in the integrated scenario was to to incorporate likely future policies, with as policy drivers three factors influencing transport markets, namely climate policy, fossil fuel scarcity and new technologies. Also a fast recovery scenario for the economic crisis was included where GDP growth would continue to normal by 2012.

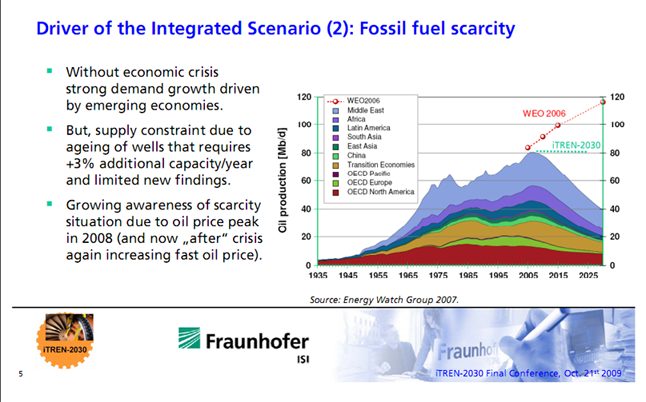

With respect to fossil fuel scarcity the project leader, Dr. Wolfgang Schade from the Fraunhofer Institute for Systems- and Innovation Research (ISI), presented two scenarios, one from the World Energy Outlook 2006 of the International Energy Agency, and the other from the Energy Watch Group from 2007. He made the remark that supply constraints due to aging wells require +3% of additional capacity per year while new discoveries have been limited. This figure is almost certainly too low given that three sources have independently from each other concluded that annual average declines are around 4.5% (CERA 2007, IEA 2008, Hook et al. 2009). Given the wide divergence of opinions over the issue of oil scarcity it must have been difficult for the consortium to decide upon which oil production scenario to take. In the iTREN-2030 project a choice was made to keep oil production at a plateau from 2005 until 2030, neither declining nor increasing. Shown in figure 5 below.

Figure 5 - iTREN-2030 slide on fossil fuel scarcity driver, Source: iTREN-2030 final workshop presentation

As to new technologies the project focused on five developments: 1) Biofuels, 2) fuel efficiency, 3) available alternative technologies including hybrid vehicles, compressed natural gas vehicles (CNG) and LPG powered vehicles, 4) Battery electric vehicles and hydrogen fuel cell vehicles, 5) New transport means including electric bikes, electric scooters, and segways. These developments were based on changes seen today that will accelerate.

Many European policies were incorporated. For Transport these included transport pricing for trucks on interurban networks after 2020, charging cars on interurban networks after 2025, city tolls for peak pricing after 2025, harmonization of fuel taxes, inclusion of air transport in the EU-ETS, liberalization of the railway system, CO2 regulation for cars (130 gCO2/km in 2015, 105 gCO2/km in 2020), CO2 regulation for light duty vehicles (170 gCO2/km in 2015, 150 gCO2/km in 2020), battery electric support leading to electric cars entering the market of city cars after 2012, and electric light duty vehicles for urban delivery after 2015, enforced implementation of CNG fueling stations, effective car labeling, regulation to use HDV low resistance tyres. Also all large scale European infrastructure road and rail projects were included by using TRANS-tools.

For Energy the policies included, 20% greenhouse gas emissions reduction by 20% in 2020 against 1990, 20% renewable energy in the final energy mix until 2020 (including 10% biofuels), the measures in the energy efficiency action plan of the European Commission and the deployment of demo-power plants for Carbon Capture Sequestration.

Results of the Integrated Scenario

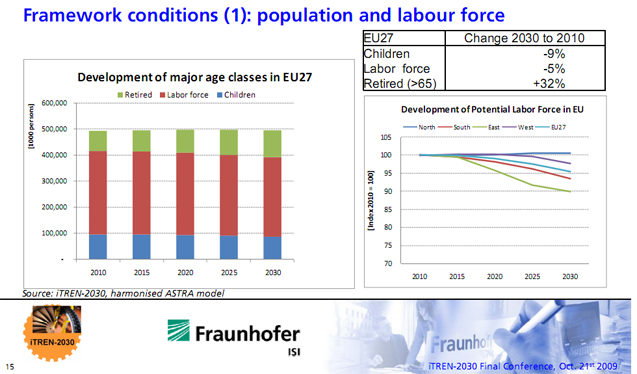

Population and GDP developments in the integrated scenario were first shown in the workshop. Population and labour force developments, show a relatively stable population up to 2030 and a decline in the labor force by 5% from 2010 to 2030 due to demographics as the number of retired people increases by 32%, shown in figure 6.

Figure 6 - iTREN-2030 slide on population and labour force in the integrated scenario, Source: iTREN-2030 final workshop presentation

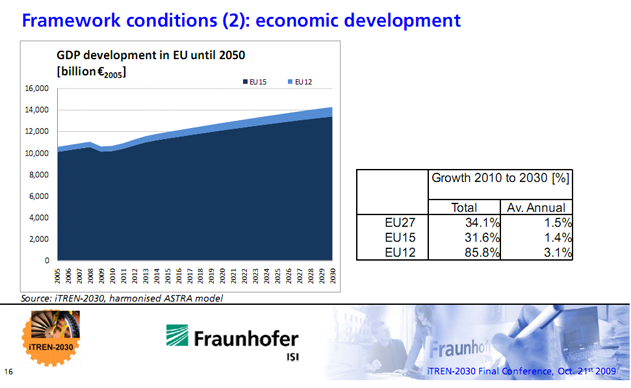

As to GDP, assumptions were inserted that the current economic crisis will be V-shaped and that a fast recovery will occur. In the integrated scenario the European Union is back to a constant growth pattern from 2012 to 2030. Growing at an average annual rate of 1.5% in EU-27, shown in figure 7. The total effect as modeled here is a 6.3% loss in GDP in 2010 versus a situation with continued growth from 2005 onwards, and a loss of 3.8% in 2030 versus a no crisis scenario.

Figure 7 - iTREN-2030 slide on GDP developments in the integrated scenario, Source: iTREN-2030 final workshop presentation

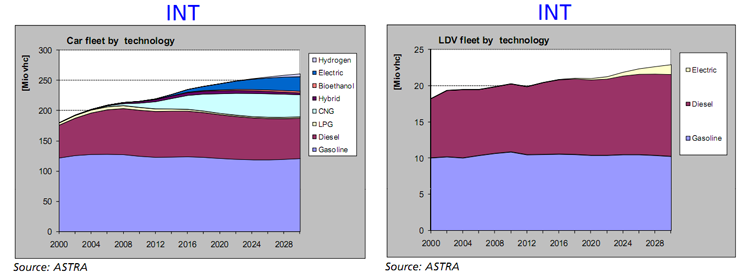

Although maritime and air developments were also shown I focus here on road transport as most changes occurred in road transport in the integrated scenario. The development of car fleets looked very promising under the assumptions used. Due to the assumption that oil production remains stable until 2030, oil price in the scenario rose to 90 euro per barrel and remained around that level until 2030. Combined with a stable GDP development this resulted in smooth technological developments. A large increase in the efficiency of cars (both diesel, gasoline as well as new technologies). This made it possible for the car fleet to grow while oil usage declined. An overall decline in oil consumption in transport (mainly due to less oil usage in car transport) of 0.1% was noted. The car fleet grows to 260 million in 2030 from around 205 million in 2005 as motorization takes off in Eastern Europe. The growth was filled in by new technologies, however, and my guess is although this was not shown, displacement of oil usage from Western to Eastern Europe. In total the integrated scenario shows a growth to 35 million compressed natural gas cars in 2030, a take-off of electric cars to 25 million in 2030, and the introduction of hydrogen vehicles by 2025. Also 3 million pure bio-ethanol cars would be on the road in 2030 The total number of Diesel and Gasoline cars declined from 200 million in 2008 to 190 million in 2030. And these cars (purple and purplish blue in figure ![]() also run up to a certain percentage of biofuels.

also run up to a certain percentage of biofuels.

Light Duty Vehicles benefit also from high oil prices by increasing efficiency, and the take-off of electric vans and light trucks by 2018 resulting in 2 million of these vehicles by 2030. In total oil driven light duty vehicles increase from 20 million in 2008 to 21 million in 2030.

Figure 8 - iTREN-2030 slide on car and light vehicle developments in the integrated scenario, Source: iTREN-2030 final workshop presentation

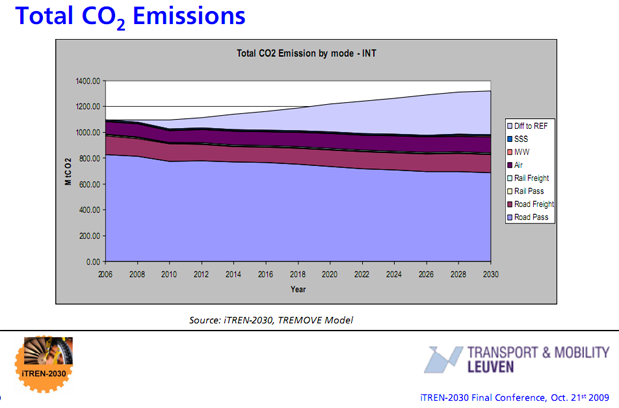

If these changes occur in the road sector it will lead to a significant decline in CO2 emissions in the overall European transport sector as shown in figure 9. Despite increases in total freight kilometers by 33.9% or 1700 to 2450 billion tonne kilometer from 2010 to 2030, and an increase by 25.7% or 4400 to 5500 billion passenger kilometers from 2010 to 2030 in cars. According to the iTREN-2030 team the European Union is steering towards a trend-shift in emissions against a ‘business as usual’ reference scenario shown in the light purple bar on top in figure 9.

Figure 9 - iTREN-2030 slide on CO2 emissions in the integrated scenario, Source: iTREN-2030 final workshop presentation

Conclusions from the iTREN-2030 team

The iTREN-2030 team concluded the workshop with several interesting conclusions here reproduced from the presentations:

About CO2 emissions:

-In the integrated scenario total CO2 emissions from transport decrease due to declining emissions from road transport.

- Rail CO2 emissions continue to increase but at a lower growth rate, and only Air transport CO2 emissions continue at relatively the same pace of growth.

About economic growth:

- Economic growth is expected to be lower than in the past (less than 2% versus more than 2% before the economic crisis),

- In a fast recovery scenario around 4 years is needed to achieve the pre-crisis economic level.

- The impact of the economic crisis provides additional time to solve problems and foster the break-in-trends.

- Dr. Wolfgang Schade the project leader however put his doubts at whether this is such a realistic scenario by saying “This assumes that the financial crisis is solved - is it solved permanently? There are signs that we are building up the next bubble.”

About vehicle fleets:

- Savings achieved by increasing fuel efficiency of passenger cars compensates expenditures for road charges.

- Average CO2 emissions of the EU-27 fleet until 2030 indicate that measure of the integrated scenario are not sufficient as only a level of 140 gram of CO2 per kilometer is reached in 2030 (versus a policy goal of 105 g cO2 per kilometer in 2020.

- Despite breakthroughs of battery technology, the potential of electric cars for long distances is supposed to be limited.

- Motorisation in EU-12 (Eastern Europe) reaches the EU-15 (Western Europe) level in 2030.

Reflecting on transparency and modeling limitations

I conclude with some personal reflections on the final workshop and the models. It was great to see many people from the European Commission (DG-TREN) and knowledgeable stakeholders being closely involved and openly reflecting on the process at the final workshop. This type of approach, where models are constructed to aid policy makers, and policy makers and knowledgeable parties are involved in the process, is in my opinion a necessity to deal with the complex problems that we face. I can only hope that such an approach will be more embedded in political decision making at the national level of my country, the Netherlands. I do think that more room needs to be given in these type of workshops to limitations and uncertainties. As in the end I did leave the workshop with a feeling that the modeling exercise did not properly addressed this. Although the purpose of iTREN-2030 was not to create the best possible scenario but to integrate the four models and show the possibilities of a scenario with likely policies, the integrated scenario did show the limitations that are inherent in the current model setup. These cannot be solved by simply altering some variables of the models, hence it is relevant in light of the main goal of iTREN-2030. Specifically I here mention three areas of importance that from my point of view need to be addressed in the future.

1) POLES the energy supply part of iTREN-2030 models energy supply from a neo-classical economic point of view. Higher prices resulting in more reserves and a gradual shift from conventional to unconventional production. Looking purely at reserves from a price perspective ignoring energy costs of production, and ignoring production flows constraints due to physical (water, materials, labour force) or political (lack of market access, oil production cap policies in OPEC countries) limitations. The iTREN-2030 project team wisely has steered around this limitation by imposing a scenario where oil production does not increase up to 2030. However this is only a partial solution. Better supply modeling can be done by either creating a new model, or augmenting the power of POLES to forecast supply by integrating physical and political production factors, oil & gas industry cycles, and energy costs of production (Energy Return on Energy Invested). Also I think more feedback needs to be created in the POLES model although based on the limited information available on POLES this may be an incorrect perception.

2) Macro-economic effects of high oil prices appear to be incorporated in a limited fashion given that GDP growth continues in a smooth fashion until 2030 after the fast economic crisis recovery. We know from several studies conducted independently that the United States economy is not able to bear oil prices much above 80 to 100 dollars per barrel. At a global oil price of 90 euro’s per barrel until 2030, or around 140 dollars per barrel, as endogenously determined in iTREN-2030, it becomes extremely unlikely that the global economy can continue to grow in a smooth pattern, and hence that the European Union economy continues to grow smoothly at around 2% per year. At the least a more shock like pattern will occur as the United States economy gets hammered by these high prices and this effect ripples through the global economy. From my perception this effect will continue until a different country/economic bloc is able to replace the role of the United States in the world economy or until the rules/system of the economic game have changed significantly.

3) A more fundamental macro-economic question lies in the world situation on the relationship between our debt based economies and limits to energy production growth. When assuming a limit to oil production growth to 2030 in the Integrated Scenario, will economies still be able to service the global debt bubble? Estimated by Hannes Kunz of IIER to be around 345% of global GDP (chart). According to his needed estimates needed GDP growth in the world economy is 6.9% to be able to create an average real return on investments of 2%. Under an oil constrained future scenario debt will become too big of a burden and the world economy will have to inflate or deflate. Certainly smooth GDP growth is out of the question if the debt bubble bursts.

Finally, I wish the European Commission the best of wisdom in creating the white paper on transport. An area that is of huge importance in my perception of an oil scarce world.

References

CERA, 2007. Finding the Critical Numbers: What are the Real Decline Rates for Global Oil Production?, Cambridge Energy Research Associates, 21 pages.

IEA, 2008. World Energy Outlook 2008, International Energy Agency Publications, Paris France, 569 pages.

Hook, M., Hirsch, R., Aleklett, K., 2009. Giant Oil Field Decline Rates and Their Influence on World Oil Production, Energy Policy, Volume 37, Issue 6, June 2009, Pages 2262-2272.

![]()

Drumbeat: October 30, 2022

U.S. natural gas rig count climbs 3 to 728 for week

The U.S. natural gas drilling rig count has gained in 13 of the last 15 weeks after bottoming at 665 on July 17, its lowest level since May 3, 2002, when there were 640 gas rigs operating.

But the rig count is still down sharply since peaking above 1,600 in September of last year, standing at 824 rigs, or 53 percent, below the same week in 2008.

Many gas producers have scaled back drilling operations with credit still tight and natural gas prices around $4 per million British thermal units (mmBtu), off nearly 70 percent from July 2008 highs above $13.

The recession is dead … long live the recession!

The world’s first peak-oil recession has come to a close, according to third-quarter numbers invented by the federal government. Apparently dumping trillions of dollars onto big banks, insurance companies, and automobile manufacturers interrupted the plummeting descent of American Empire. The stock markets skyrocketed expectedly. Predictably, so did the commodities markets.

In fact, the lifeblood of western civilization is bumping up against the “Goldilocks” limit of $80/bbl, as I predicted would occur under economic growth. A minimum price of $60/bbl allows oil suppliers to make enough money to justify new projects, so per-barrel prices between $60 and $80 are supposed to be “just right,” even though today’s price is four times higher than the 20-year average. The “Goldilocks” minimum price of $60/bbl matches the “Goldilocks” maximum price of 2005. As recently as 2003, OPEC had an official “Goldilocks” zone between $22/bbl and $28/bbl. For a little historical context, consider this: In 1969, the U.S. refused a ten-year, locked-in offer of $1/bbl oil from the Shah of Iran because the price was too high.

The story of gas (5)

Russia’s gas production, though currently in decline, is expected to experience a boost of up to 40 percent over 2008 by the year 2030.

Still, it is natural gas from Central Asia and the Caspian that is of crucial importance for both Nabucco and South Stream, while unimpeded access to these resources will finally decide which of the two pipelines could become a viable gas exporting route. After all, every race has a winner and a loser.

Shortage of natural gas in the Middle East could impact new petrochemical projects

Increased domestic gas demand, delayed supply response, limited regional pipeline co operation, and below-market pricing are factors that affect the long-term security of gas supply here. Evolution of the region’s gas industry has lagged behind that of the oil sector, despite significant gas deposits. Gas was traditionally weaker than crude oil in the Gulf, and suffered from persistent under investment in the 1990’s because there was no financial incentive to upgrade infrastructure. Also, the Middle East region is not uniformly gas rich- Qatar, Iran, Egypt and Saudi Arabia have significant gas reserves, while others like the UAE, Kuwait, Bahrain, Jordan and Syria are relatively gas-poor. Oman and Yemen have chosen to export gas that could otherwise satisfy long term domestic demand. Further, gas reserves alone do not result in available gas supply, as seen in Iran’s inability to become an important gas exporter despite its enormous reserves, and limitations faced by Iraq for successful gas development. Since much of the region’s gas supply is associated gas rather than non-associated gas, reserves are often not available to supply domestic markets or export markets because re-injection is critical to maintain current levels of crude oil production.

Polish firm agrees deal to import more Russian gas

WARSAW (Reuters) - Poland’s gas monopoly PGNiG PGNI.WA and Russia’s Gazprom agreed on increased gas deliveries to Poland under a deal that will run until 2037, PGNiG said on Friday.

The deal, which still needs to be approved by both governments, follows months of negotiations between Poland and Russia and lessens risk of winter gas shortages in the ex-communist European Union member country.

ConocoPhillips Shifts to a Leaner Strategy

ConocoPhillips CEO James Mulva signaled a dramatic shift in course for the nation’s third-largest oil company Wednesday, saying that after years of bulking up through acquisitions, it is now focused on being a smaller, leaner business that takes better care of its shareholders.

“Some will say what we’re doing essentially is that we’re shrinking to grow,” Mulva said during a conference call to discuss the company’s quarterly earnings. “That would be a fair assessment.”

But the change is necessary in light of the global recession and the difficulty of accessing new oil and gas reserves around the globe, coupled with the massive costs of extracting them, he said.

The Philippines: Open books to gain sympathy, oil firms told

A MALACAÑANG official yesterday oil companies should not expect to gain public sympathy unless they open their books.

Gary Olivar, deputy presidential spokesman for economic affairs, said oil companies should quit hiding behind the Oil Deregulation Law and be more transparent, more cooperative and comply with the policies of government.

Egypt’s nuclear plans threatened

CAIRO // As Egypt’s government prepares to finalise plans for the country’s first nuclear power plant by the end of this year, opposition from a prominent tourism developer risks scuttling the project.

But if the proposed site at Al Dabaa, a remote strip of desert coast about 140km west of Alexandria, does not receive final approval by the end of this year as planned, it could spell the end of Egypt’s nascent civil nuclear energy plans and the beginning of an energy crisis, said Mohamed Mounir Megahed, the vice chairman for the Nuclear Power Plants Authority.

Nicaragua taps geothermal energy with Canadian firms

MANAGUA, Nicaragua (UPI) — Nicaragua is hoping to tap into its vast geothermal power resources and has awarded two concessions to Magma Energy Corp. and its partner Polaris Geothermal Inc., both of Canada, as part of a long-term energy self-sufficiency plan.

Industry experts say Nicaragua has the most geothermal energy potential of any country in Central America. Mostly trapped in volcanic mountains along the Pacific Coast, experts say geothermal energy alone can solve Nicaragua’s energy crisis while efforts are under way to exploit wind power and other forms of renewable energy.

Asian car manufacturers among leaders in “world sustainability league”

Asian car manufacturers are outperforming their American and several of their European rivals in using their economic, environmental and social resources more efficiently.

An open letter to Steve Levitt

The problem of global warming is so big that solving it will require creative thinking from many disciplines. Economists have much to contribute to this effort, particularly with regard to the question of how various means of putting a price on carbon emissions may alter human behavior. Some of the lines of thinking in your first book, Freakonomics, could well have had a bearing on this issue, if brought to bear on the carbon emissions problem. I have very much enjoyed and benefited from the growing collaborations between Geosciences and the Economics department here at the University of Chicago, and had hoped someday to have the pleasure of making your acquaintance. It is more in disappointment than anger that I am writing to you now.

I am addressing this to you rather than your journalist-coauthor because one has become all too accustomed to tendentious screeds from media personalities (think Glenn Beck) with a reckless disregard for the truth. However, if it has come to pass that we can’t expect the William B. Ogden Distinguished Service Professor (and Clark Medalist to boot) at a top-rated department of a respected university to think clearly and honestly with numbers, we are indeed in a sad way.

Arctic Sediments Show That 20th Century Warming Is Unlike Natural Variation

ScienceDaily — The possibility that climate change might simply be a natural variation like others that have occurred throughout geologic time is dimming, according to evidence in a Proceedings of the National Academy of Sciences paper published October 19.

The research reveals that sediments retrieved by University at Buffalo geologists from a remote Arctic lake are unlike those seen during previous warming episodes.

The UB researchers and their international colleagues were able to pinpoint that dramatic changes began occurring in unprecedented ways after the midpoint of the twentieth century.

Willing to give up blue skies for climate fix?

We can probably engineer Earth’s climate to cool the planet, scientists say, but are we willing to live with the downsides? Those could include creating more droughts, more ozone holes and, oh yeah, a thin cloud layer that obscures blue skies and gives astronomers fits.

With potential negatives like that it’s no wonder that “geoengineering,” as the technique is called, has few hardcore advocates.

White House fights back on Cash for Clunkers

Obama administration goes to battle with Edmunds.com on Cash for Clunkers analysis, saying the program contributed heavily to last quarter’s economic expansion.

Putting Up Produce: Yes, You Can

The worst recession in decades and a trend toward healthier eating are inspiring many Americans to grow their own food. Now the harvest season is turning many of these gardeners into canners looking to stretch the bounty of the garden into the winter.

From farm to table, a link to the past

The event is part of a larger program called RAFT Grow-Out. RAFT, which stands for Renewing America’s Food Traditions, is affiliated with Slow Food USA and made up of many smaller organizations dedicated to what RAFT calls the “save it by eating it’’ paradigm. The Grow-Out, held for the first time, provides farmers with donated heirloom seeds and connects them to chefs who create menus based around the crops. Boston-based nonprofit Chefs Collaborative is the RAFT partner working with this event. Participating restaurants include Henrietta’s Table and Hungry Mother, both in Cambridge, and Tastings Wine Bar and Bistro in Foxborough.

Renewed interest in heirloom foods stems from a variety of factors. Some chefs like the taste of antiquated squash, others want to preserve crop diversity as a matter of food security.

Three Gorges Dam ‘a model for disaster’

China’s Yangtze River hydropower project has been a ‘model for disaster’, according to a river protection charity, which is concerned about new proposals for similar projects.

The Three Gorges Dam, whose reservoir is due to reach its final height of 175 metres over the next few weeks, will be able to produce enough electricity to meet close to one tenth of China’s current electricity demands.

However, Rivers International say the Dam has driven fish species to extinction, caused frequent toxic algae blooms and is subjecting the area to erosion and frequent landslides.

EPA requires AEP to test W.Va. coal-ash site

CHARLESTON, W.Va. (AP) — The U.S. Environmental Protection Agency said Thursday it is requiring American Electric Power to conduct safety tests on waste impoundments at a West Virginia coal-burning plant to ensure their structural stability.

Although the impoundments at the Philip Sporn plant aren’t considered an immediate failure risk, EPA said it was requiring the tests because the structures have similar designs to one that failed last December in Tennessee.

City puts bicyclists directly in the path of motorists

In one of the busiest shopping districts in Long Beach, Calif., bicyclists are kings of the road in an experiment that turns frustrated motorists into serfs.

The seaside city south of Los Angeles is encouraging bikers to get right in front of cars. It painted a five-foot wide green stripe down the middle of one of the two lanes in either direction of the Belmont Shore section of the city. Even though cars were whizzing by at 30 miles an hour yesterday, bikes were free to ride right in their path.

Saudis to drop WTI as price benchmark for U.S. crude

The U.S. share of world crude use has fallen to less than 23 per cent in 2008 from 26 per cent in 2001.

In the past year, it has fallen by another 750,000 barrels a day, or 3.7 per cent. Countries such as China and India are expected to dominate future growth in oil demand.

As a result, the pricing of the U.S.-based WTI has begun to decline in importance. Although Argus is also a U.S. price, it is more closely linked with international oil and is seen as a more reliable indicator of global oil prices.

“What it [the Saudi move] really speaks to is the demand shift in oil away from the U.S. and to other places in the world. That’s what’s really driving the bus,” said Jeff Rubin, the former CIBC chief economist and author of Why Your World Is About to Get a Whole Lot Smaller: Oil and the End of Globalization.

“North American oil demand has peaked,” he said. “What this really says is that whereas WTI in the past had been a premium price, now WTI is going to be a discount price.”

Aramco to drop WTI as pricing guide for crude

Aramco’s switch to ASCI sparked speculation other exporters of sour crude to the US may follow its example. But the move should not be interpreted as a rejection of WTI’s general role as market leader, Horsnell said. “US gulf crudes tend to be assessed in terms of differentials to WTI, rather than as separate centers of independent price discovery, and we expect that to continue,” he said. “Should an active OTC or futures market based on ASCI eventually arise, then the dynamics could change. However, establishing futures contracts based on delivered US gulf sours has proved very problematic in the past and is still very far from an inevitable development. Indeed, the current regulatory climate is not exactly ideal for any innovative development of new OTC or formal exchange-based oil derivatives.”

SNAP ANALYSIS - Saudi switch aims for better value for its oil

DUBAI (Reuters) - Saudi Arabia is dropping a U.S. light sweet crude oil benchmark as the basis for pricing its sales to the United States for one more like its own sour crude and that is less swayed by the volatile futures market.

NYMEX plans two new sour crude futures contracts

NEW YORK (Reuters) - The New York Mercantile Exchange plans to launch a cash-settled futures contract tracking the Argus sour crude index by year end and another contract for physical delivery sour crude at a later date, NYMEX operator CME Group said on Thursday.

CME said the NYMEX contract plans are a response to Argus Media’s announcement on Wednesday that Saudi Arabia’s state oil company Aramco will switch to the Argus sour crude index as the benchmark price for all grades of crude sold to the United States.

Matt Simmons: ASPO’S Peak Oil Message: Successes And Impediments

Daniel Yergin on What’s Next For Global Energy

Perhaps no one is better positioned to sift through the complicated and interrelated questions surrounding “peak oil,” renewable energy, climate change and energy security, than Cambridge Research Energy Associates Chairman Daniel Yergin.

Yergin won a Pulitzer Prize for his book, The Pize: The Epic Quest For Oil, Money & Power, published nearly twenty years ago - and has recently written a new epilogue for the book on the current state of the great energy game.

Yergin will be sitting down for a chat on the future of global energy with Steve Clemons today from 12:30pm - 2:00pm at the New America Foundation.

Putin Warns Ukraine Over Gas Crisis

NOVO-OGARYOVO, Russia (Reuters) - Russian Prime Minister Vladimir Putin on Friday warned that Ukrainian President Viktor Yushchenko risked provoking a new gas crisis that could disrupt supplies to Europe.

“It looks like, we will again have problems with energy payments,” Putin said after a telephone call with Ukrainian Prime Minister Yulia Tymoshenko, Yushchenko’s main political foe and a frontrunner in a January 17 presidential election.

Gazprom in Europe: Russian government plans to share part of Yamal gas resources

The Russian government plans to share bits of the giant Yamal prize with international companies. However, rather than a sign of liberalism, this represents an attempt to address the fundamental challenges that the expanding Gazprom is facing in Europe.

Chevron Third-Quarter Profit Declines as Energy Demand Slumps

(Bloomberg) — Chevron Corp., the second-largest U.S. energy company, said third-quarter profit fell 51 percent as slumping fuel demand pulled down oil and natural-gas prices.

12 dead in Jaipur oil depot blaze; Deora says fire ‘to die down on its own’

JAIPUR: Petroleum minister Murli Deora on Friday said the fire at Indian Oil Corporation’s fuel depot on the outskirts of the city has to die down on its own and there was “no other solution” to douse the leaping flames.

SEG: Saleri says oil, gas key in new energy era

HOUSTON — The world has entered a new energy era in which overall energy efficiency and oil recovery efficiency will improve, environmental harmony will grow, and oil, gas, and coal will continue to dominate.

That is the view of Nansen Saleri, founder, president, and chief executive officer of Quantum Reservoir Impact LLC, Houston, and a former Saudi Aramco reservoir management chief.

When considering conventional and unconventional resources, 150-250 years of liquids production remain at output levels of 50-100 million b/d, Saleri said, relying on National Petroleum Council 2007 estimates.

Global oil recovery factors long estimated at around 35% have begun growing toward 50-60% and will ultimately reach 80%, he forecast in a presentation to the Society of Exploration Geophysicists annual meeting in Houston.

The energy world is filled with unpredictability over the outcomes of recession, price volatility, geopolitics, resource nationalism, renewables, global warming, and most of all “peak oil” versus peak demand.

Geophysicists and the rest of the oil and gas industry should focus more on peak demand than on peak oil, Saleri urged.

Exxon, Oil Majors Battle to Restore Earnings as Demand Plunges

(Bloomberg) — Exxon Mobil Corp., PetroChina Co. and Royal Dutch Shell Plc are battling slumping fuel demand as oil majors seek to rebuild profits battered by the global fallout from the worst U.S. downturn since the Great Depression.

Exxon Mobil’s U.S. refineries lost about $2.3 million a day last quarter as gasoline and diesel prices fell. Shell, whose refining earnings declined 47 percent, said the plunge in demand will keep profit margins narrow in “the short and medium term” and a quick recovery in energy usage and prices is unlikely.

Oil companies around the world are slashing costs, cutting jobs and holding back on some new investment to halt the slide in earnings, even as they seek to fund renewable energy projects. Exxon Mobil cut its capital-spending estimate for 2009 by 10 percent as third-quarter profits at the Irving, Texas- based explorer and Shell hit their lowest level in six years.

Oil companies give cool outlook

LONDON (Reuters) - Exxon Mobil Corp, Royal Dutch Shell Plc and Eni SpA dashed hopes for an imminent turnaround for the oil industry, saying sluggish economic recovery was weighing on energy demand and prices.

The three posted big drops in quarterly earnings on Thursday after crude oil and natural gas prices plummeted and refining margins were squeezed.

India’s Reliance Industries Q2 profit dips 6.55 pct

MUMBAI (AFP) – Indian refining and energy giant Reliance Industries Ltd said quarterly net profit dropped by 6.5 percent on Thursday as core refining margins fell following a tumble in global crude prices.

Saudi move is bid to realign oil market

LONDON (Reuters) - Saudi Aramco’s decision to abandon a light sweet oil benchmark closely linked to NYMEX futures as the basis for crude sales to U.S. customers reflects growing frustration with its performance over the last two years.

While it will not imperil NYMEX’s status as the main forum for oil futures trading, it will increase pressure on the exchange to consider adjustments to its contract. In time NYMEX may have to allow a wider range of crudes to be delivered and add a delivery location on the U.S. Gulf Coast.

Senate Panel Backs Iran Petroleum Investment Sanction

(Bloomberg) — The Senate Banking Committee voted unanimously today to further restrict trade with Iran and impose sanctions on companies that help the country acquire refined petroleum products.

The 23-0 vote follows yesterday’s approval by the House Foreign Affairs Committee of a similar measure to sanction companies involved in supplying, shipping, financing and consulting for Iran’s petroleum sector. Iran has limited refining capacity.

Chevron tried to taint Ecuador toxic waste trial: lawyer

WASHINGTON (AFP) – Videos posted online by US oil company Chevron purporting to show rampant corruption among Ecuadoran officials are actually a set-up meant to taint an ongoing trial against the energy giant, an attorney in the case alleged.

“By releasing the videos, in my opinion Chevron is trying to taint a trial process that they knew they were going to lose, with the hope that the case would be dismissed in Ecuador,” Steven Donziger, an attorney for Ecuadoran Amazon communities who are suing the oil giant told reporters.

Russia Cuts November Crude Oil Export Duty by 3.9%

(Bloomberg) — Russia’s government will cut the export duty on crude oil by 3.9 percent on Nov. 1, according to an order signed by Russian Prime Minister Vladimir Putin.

The levy will decrease to $231.20 a metric ton, or $31.54 a barrel, from $240.70 a ton the previous month under the order, which was published today in the official Rossiyskaya Gazeta newspaper.

Gazprom Sees Europe Gas Demand In 2020 Up 12.5% To 700 BCM/Year

LONDON -(Dow Jones)- Russia’s state-controlled natural gas monopoly OAO Gazprom expects annual demand for gas in Europe to grow to 700 billion cubic meters in 2020, up 12.5% from the current level, the company said in a statement late Thursday.

Dead fish drifting in Indonesia after oil leak

JAKARTA, Indonesia – Thousands of dead fish and clumps of oil have been found drifting near Indonesia’s coastline more than two months after an underwater well began leaking in the Timor Sea, officials and fishermen said.

An estimated 400 barrels a day of oil has been leaking from a fissure that erupted on Aug. 21 at a rig about 150 miles (250 kilometers) off the Australian coast. PTTEP Australasia, a branch of Thai-owned PTT Exploration and Production Co. Ltd., has failed repeatedly to stop the leak but says it is still trying.

Canada’s Economy Unexpectedly Shrank 0.1% in August on Energy

(Bloomberg) — Canada’s economy unexpectedly shrank in August, suggesting the economy may not have exited a recession in the third quarter after output was little changed in July.

Gross domestic product fell 0.1 percent in the month, as oil and gas extraction dropped 2.3 percent and manufacturing fell 0.7 percent, Statistics Canada said today from Ottawa. Economists expected a 0.1 percent increase, according to the median estimate of 23 analysts surveyed by Bloomberg.

The Next Economic Crisis, Spiralling Inflation

Peak Oil is not someone’s pet theory. It is not a rumour spread by left-leaning conservationists. Peak Oil is supported by hard production data. Peak Oil is a field-by-field extrapolation of what has already happened to existing oil fields. As most investors know, the US has had to import ever-increasing amounts of oil as their own supplies have decreased. But now, the exact same thing is happening in Britain’s North Sea and in Mexico.

Oil is a finite resource, and many of the world’s largest oil fields are being rapidly depleted. The maximum rate of global petroleum extraction has peaked, and now the rate of production is entering terminal decline. The reason for the decline is, to a large extent, the lack of new discoveries. Most of the major discoveries were made in the 1950s and 1960s. Since then, the annual discoveries of oil have kept dropping to the point where, when we take oil out, we do not replace the reserves.

ConocoPhilips: Time to Embrace Natural Gas Transportation

Since the shale plays have been, and will continue to be, a game changer in this space, why doesn’t Mulva join other natural gas advocates like Hefner, Pickens, and McClendon and embrace natural gas transportation in America? Certainly COP will continue to profit from the fundamentals of oil supply/demand and the continuing ramping up of gasoline powered vehicles in China, India and Asia in general. This is validated by a $75/barrel price during a period of brimming oil inventories coincident with the worst financial downturn since the Great Depression.

India grants Congo $263 mln in infrastructure loans

KINSHASA (Reuters) – India has offered Democratic Republic of Congo $263 million in loans to build hydroelectric plants and repair battered infrastructure in the war-ravaged central African nation, Congo’s foreign minister said on Friday.

Canadian Hydro drops plan to buy Lake Erie wind farm

Calgary-based Canadian Hydro Developers Inc. said Friday it has terminated its earlier plans to purchase a subsidiary that is developing one of the largest wind farms in the world in Ontario.

The company had first agreed to the deal with Utah-based Wasatch Wind Inc. for the rights to the 4,400 megawatt project, to be built in Lake Erie, at the beginning of October. Terms of the deal had not been disclosed.

However Canadian Hydro has since been acquired by TransAlta Corp., leading to the change in strategy.

Local Motors: A New Kind of Car Company

When John B. Rogers was a Marine deployed in Iraq in 2004, he brought a book called Winning the Oil Endgame with him to the Gulf. The book, by environmental activist Amory B. Lovins, discusses how people can end their dependence on fossil fuels. Rogers says reading the volume inspired him to create a new type of car company, one he believes offers a more efficient and effective way of designing, manufacturing, and selling autos.

New energy = new transmission lines: But finding agreement on where to put them isn’t easy

DENVER — Giant wind turbines and solar collectors have become the icons for our great energy transition from fossil fuels to renewable sources. But will giant electrical transmission lines ever become half as sexy?

Chinese banks to fund $1.5B Texas wind farm

China took a big leap into the U.S. renewable energy market Thursday, putting up $1.5 billion for a 36,000-acre wind farm in Texas with the power to light up 180,000 homes.

The project is a joint venture with U.S. Renewable Energy Group, a private equity firm, Austin, Texas-based Cielo Wind Power LP and Shenyang Power Group of China.

Solar power execs bullish on 2010 despite earnings

ANAHEIM, California (Reuters) - Executives from solar power companies see clearer skies in 2010 for the beleaguered industry, even as quarterly reports from heavyweights like First Solar Inc and SunPower Corp have disappointed investors and dragged down shares.

The industry has struggled to emerge this year from tight credit markets, a global glut of panels and falling prices.

BP Is ‘Disappointed’ With $87 Million Texas City Refinery Fine

(Bloomberg) — BP Plc, which expects an $87 million fine in relation to its response to an explosion at the Texas City refinery, said it’s “disappointed” with the penalty from the U.S. Occupational Safety and Health Administration.

OSHA this month rejected BP’s request for more time to comply with a settlement over the 2005 blast, which killed 15 workers and left hundreds injured. The London-based company, Europe’s second-largest oil producer, now anticipates a fine, spokesman Andrew Gowers said today by phone.

Argentine enviro secretary fined for dirty river

BUENOS AIRES, Argentina – Environmentalists praised a judge on Wednesday for fining Argentina’s environmental secretary and two local politicians for failing to clean up the polluted river that flows sluggishly through the heart of the capital.

Tests on treasured maize ignite fears in Mexico

MEXICO CITY (AFP) – As scientists race the clock to increase food production worldwide, new trials to plant genetically-modified maize have stoked anger in Mexico, the cradle of corn.

Many here are sensitive about meddling with maize, which dates back to pre-Hispanic times, when mythologies held that people were created from corn.

Some fear Mexico could one day lose the wealth of native varieties it still produces, including red and blue, to a few, tough breeds of GM maize, as well the livelihoods of hundreds of thousands of subsistence farmers.

Will U.S. go empty-handed to world climate talks?

WASHINGTON — Without a new law requiring cuts in greenhouse gas emissions, the U.S. could end up going empty-handed to the international climate talks in December.

Many nations are watching to see whether the Senate will make progress on a climate and energy bill that would spell out the U.S. national emissions-reduction plan. Without an offer of such cuts from the largest source of emissions that are already in the atmosphere, there won’t be a global deal at the talks in Copenhagen, Denmark .

EU sets 100 bln euro climate summit goal for poor states

BRUSSELS (AFP) – EU leaders were struggling Friday to agree how to fund the fight against climate change, with poorer eastern European nations urging their more affluent western neighbours to bear the lion’s share of the burden.

China, India could shame rich nations: UN scientist