Renewables & efficiency - Apr 29

-Giant gravel batteries could make renewable energy more reliable

-Giant gravel batteries could make renewable energy more reliable

-Regulators Approve First Offshore Wind Farm in U.S.

-Colorado Shows How It’s Done

-Windmill Boom Curbs Electric Power Prices for RWE

read more

Peak oil, prices, and supplies - Apr 29

-Peak at the polls

-Saudi Arabia global oil exports to wane post-2010

-Drilling and spilling for all the oil that’s left

-Gulf oil spill ‘five times’ larger than estimated

-Flight disruptions in Europe a Foretaste for Period of Oil Decline

-The Imminent Crash Of Oil Supply: Be Afraid

-Peak oil predictions

read more

BBC on the impact of biofuels on Paraguay’s ecology and farmers

Everyone should listen to this BBC report on the “price of biofuels.” It digs into a key question: what does Europe’s appetite for biodiesel mean for people and ecosystems in the countries that produce the feedstocks?

Everyone should listen to this BBC report on the “price of biofuels.” It digs into a key question: what does Europe’s appetite for biodiesel mean for people and ecosystems in the countries that produce the feedstocks?

read more

CityBeat Podcast 44: Wendell Berry

Philosopher-farmers Wendell Berry, Wes Jackson and Gene Logsdon discuss the future of agriculture, the environment and changing our ideas about growth and progress.

read more

Carbon Capture and Storage: Economic Costs Revisited

This is an updated version of post by Rembrandt from 2007.-Gail

Capturing carbon dioxide from coal (and gas) fired electricity plants, and subsequently transporting carbon dioxide from the plant and storing it underground in (abandoned) oil/gas fields, in other geological formations or on the ocean floor, seem like an excellent solution for continued fossil fuel use in the coming decades.

When I looked at the situation in 2007, the European Union hoped to have 12 large CO2 capture and storage demonstration projects at coal plants of at least 250 MW of capacity in place by 2015, requiring an investment of 5 billion euro. Progress has been slow, however. At the end of 2009, after 13 months of discussion, the European Union finally made the decision to invest 1 billion euro in six demonstration projects. In February, 2010 another 300 million euro was made available, which would be sufficient for two more CO2 capture and storage demonstration projects. The expectation behind these investments are that they will lead to significant cost reductions, making the technology affordable by 2020.

Even as these projects get off the ground, there are two large drawbacks:

- The process is quite energy intensive, and thus will use up coal supplies faster.

- Because of the additional energy cost the process will remain quite expensive, it is not certain that costs can be reduced sufficiently

In this post, I will talk about the second item, the high economic cost. In my previous post, I quantified the impact the extra energy cost might be expected to have on coal depletion.

In 2007, I participated in an evening group discussion about possibilities for the Dutch economy relating to capturing and storing carbon dioxide. After two interesting talks, one outlining the technical possibilities for storage in the Netherlands and the other the commercial possibilities, one of the other participants made a remark that was spot on. No matter how wonderful the idea of capturing and storing carbon dioxide may sound, it will always be costly to do so relative to current electricity production costs.

The additional costs were estimated by the IPCC in a 2007 special report on carbon dioxide capture and storage at 1 to 5 cents per kilowatt-hour (with these cents computed in US$), with the difference depending on the type of power plant, the technology employed for capturing, the reservoir in which the CO2 is stored, the transporting distance and other variables. The largest share of the costs originate from the extra energy needed to capture a pure stream of carbon dioxide for storage. The IPCC estimates the costs using a broad range of publications for different power plants as follows:

“Application of CCS to electricity production, under 2002 conditions, is estimated to increase electricity generation costs by about 0.01–0.05 US dollars per kilowatt hour (US$/kWh), depending on the fuel, the specific technology, the location and the national circumstances. Inclusion of the benefits of EOR [enhanced oil recovery] would reduce additional electricity production costs due to CCS by around 0.01–0.02 US$/kWh”

More specifically:

“The application of capture technology would add about 1.8 to 3.4 dollar cents per kWh to the cost of electricity from a pulverized coal power plant, 0.9 to 2.2 dollar cents per kWh to the cost for electricity from an integrated gasification combined cycle coal power plant, and 1.2 to 2.4 dollar cents per kWh from a natural gas combined-cycle power plant. Transport and storage costs would add between –1 and 1 dollar cents per kWh to this range for coal plants, and about half as much for gas plants. The negative costs are associated with assumed offsetting revenues from CO2 storage in enhanced oil recovery (EOR) or enhanced coal bed methane (ECBM) projects. Typical costs for transportation and geological storage from coal plants would range from 0.05–0.06 dollar cents per kWh.”

Figure 1 - Costs of Carbon Capture and Storage in dollars per kWh from the IPCC report

Figure 1 - Costs of Carbon Capture and Storage in dollars per kWh from the IPCC report

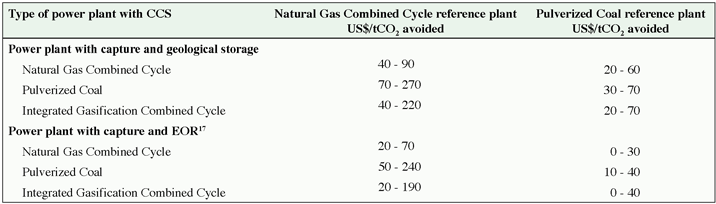

Figure 2 - Costs of Carbon Capture and Storage in dollars per ton of CO2 avoided from the IPCC report

Figure 2 - Costs of Carbon Capture and Storage in dollars per ton of CO2 avoided from the IPCC report

When I did my analysis in 2007, the industrial base price of electricity in the Netherlands was about 7 eurocents per kWh or 9.6 dollar cents per kWh. This was in the high range relative to other European countries. For the most likely application-a pulverized coal power plant-the additional cost of capture and storage would amount to 20% to 30% over and above the industrial base price. This is confirmed by a recent study to published in Energy Policy, volume 35, Issue 9, September 2007, pages 4444-4454: “Cost and performance of fossil fuel power plants with CO2 capture and storage“. The authors, E. Rubin et al, estimate a cost increase of 15% to 30%. They base this on a wide range of previous publications.

To cover these costs in the long run in a market environment, companies are looking at two distinct options. First, there is the hope that carbon capture and storage can be paid by the pricing of carbon dioxide through the European emissions trading scheme. Second, the possibility of enhanced oil recovery by carbon dioxide injection in oil fields could offset some of the costs incurred.

The European emission trading scheme is an initiative under the Kyoto protocol. It provides Europe with a market to trade greenhouse gas emission allowances or emission reduction units. Each individual company is given an assigned amount of Kyoto Protocol Units or Carbon Credits which can be increased or decreased through several mechanisms. Every carbon credit is equivalent to a reduction of one ton of greenhouse gas emissions. Within the trading scheme, a party is allowed to transfer their carbon credits to or from another party. An unlimited number of units may be acquired by emissions trading while only a limited number may be transferred to another party. At the moment, carbon capture and storage is not incorporated as a possibility for mitigation under the emissions trading scheme.

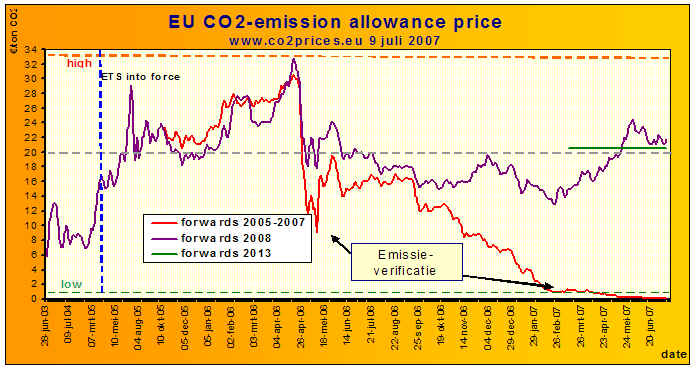

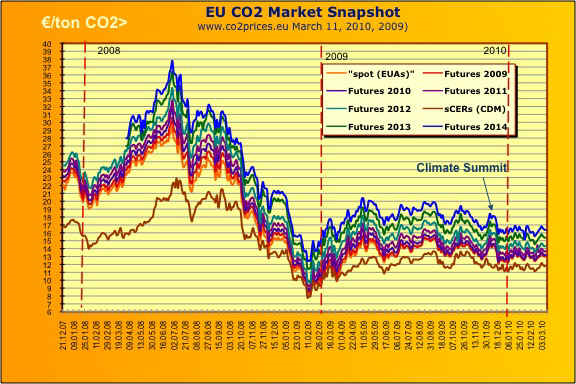

The European carbon credit market passed its test phase and became effective in 2008. During the test stage before 2008, it did not function very well because too many credits were handed out, thereby putting a downward pressure on the price of a ton of carbon. We can see this in Figure 3 below. In April 2006, when news came out that countries had a surplus of credits, their value began dropping significantly. During 2008 when more players entered the market and the market became effective, the cost of a ton of CO2 rose significantly, up towards 40 euro, but from June onwards the price dropped significantly due to investor expectations being adjusted by developing events in the economy. As the economy has only slowly picked up somewhat, and energy consumption is still low relative to early 2008 levels, the price of CO2 is still very low as shown in Figure 4 below.

Figure 3 - Price development per ton of Carbon dioxide under the European emission trading scheme, source: www.emissierechten.nl.

Figure 3 - Price development per ton of Carbon dioxide under the European emission trading scheme, source: www.emissierechten.nl.

Figure 4 - Price development per ton of Carbon dioxide under the European emission trading scheme from November 2007 to March 2010, source: www.emissierechten.nl.

Figure 4 - Price development per ton of Carbon dioxide under the European emission trading scheme from November 2007 to March 2010, source: www.emissierechten.nl.

Now, in 2010, the price for a carbon credit lies between 12 and 18 euros per ton CO2. In relation to the costs of carbon capture and storage this is much too low. In Table 2, the cost estimates from the IPCC for a pulverized coal power plant are shown to be between 30 to 70 dollars per ton CO2 or 20 to 50 euros. The present price makes the technology an economic disaster at any location. It is difficult to predict whether the price of carbon will increase because the development of the market is heavily dependent on economic developments and political negotiations. For instance, will more countries outside the European Union join in the trading in the future? Will the amount of carbon credits handed out be adjusted to the new economic situation?

Next to emissions trading, there are high hopes for enhanced oil recovery. In my opinion, these hopes are overblown, given that the technique can only be applied commercially at very few oil fields. This was recently highlighted by Statoil and Shell. The companies dropped plans to store CO2 at the Draugen oilfield in Norway because economic analysis showed that it was uneconomical to do so. Nonetheless, enhanced oil recovery is often considered as a possible option as explained in the case study below.

Pioneering Carbon Capture and Storage: Rotterdam Harbour

One of the 12 large CO2 capture and storage demonstration projects that the European Commission wants to develop by 2015 could very well be located in the Dutch harbour of Rotterdam. In 2007, the environmental agency of the Rijnmond Region, in which Rotterdam Harbour lies, calculated that it would be possible to capture and store up to 20 million tons of carbon emissions from the Rotterdam region annually for only 24 euro per ton of CO2 (PDF in Dutch, 3.6 MB, 56 pages), a price that is much lower than normal thanks to efficient usage of energy. A significant amount of heat created by local industry is wasted which can be applied for usage in the capture process. The environmental agency has assumed that this waste heat can be utilised for free as input in the capture process, hence the huge reduction in costs for capture and storage. However, it still remains to be seen whether the local companies will comply with giving away their waste heat for free-no one has asked the companies formally thus far.

In the analysis of the agency, if a price of 24 euros per ton of CO2 can be realized (which is much higher than the current trading range of 12 to 18 euros), then this project would be viable under the European emission trading scheme. Additional funding could be gained by the application of enhanced oil recovery according to the environmental agency of Rijnmond. In the agency’s analysis, they assume that two additional barrels of crude oil will be produced for every ton of injected CO2. They also assume an oil price of 30 dollars per barrel. However, this income flow is very variable. When applicable at an oil field, the injection of carbon dioxide will only be maintained for a few years. Beyond that period, it is not expected to not deliver additional production benefits, so the income flow can be expected to slow down and then come to a halt. Furthermore, time is running out, because many fields that appear to be suitable for carbon dioxide injection for enhanced oil recovery will be closed down in the period of 2008 to 2012. By 2018, very few oil fields will be available for injection purposes.

Summarizing

While the idea of carbon dioxide capture and storage seems excellent, the costs are a large hurdle that might cancel this option altogether. Only with continued political support will this technological mitigation option for climate change become viable. The best option in pursuing this technology is full support of carbon dioxide capture and storage in the European emissions trading scheme, to make pioneering projects such as the one proposed at Rotterdam harbour viable. For larger application beyond a few projects, the price of a ton of carbon needs to increase, or the costs of capture and storage will need to come down significantly. Whether this will happen in the long term future is doubtful.

![]()

BSkyB windfall hopes take shares to top of a calmer FTSE 100

• BSkyB shares jump 4.9% as markets look to News Corp move

• FTSE ends up 0.6% as Greece woes ease

• Taylor Wimpey faces shareholder resistance to pay deal

Some sense of calm returned to stock markets on Thursday as Greece’s bailout appeared within grasp and a slew of better-than-expected corporate results took attention away from fiscal woes.

A healthy dose of background jitters accompanied the apparent composure, but as signs emerged that key players were readying to approve an aid package and as Greece worked on new austerity measures to help secure the billions, the euro recovered somewhat from Wednesday’s one-year low agsinst the dollar. The US Federal Reserve also buoyed market sentiment with its view late on Wednesday that economic activity was picking up.

All that helped the FTSE 100 finish up 31.2 points, or 0.6%, at 5617.8 but it was a long way from reversing losses of more than 160 points made over the previous two sessions.

It was a packed day for company news with Spain-based bank Santander and German chemicals companies BASF and Bayer all beating the market’s expectations.

It was a similar pattern in the UK, where there were upside surprises from media group BSkyB, consumer goods firm Unilever, drugmakers Shire and AstraZeneca, hotels-to-coffee group Whitbread and miner Kazakhmys.

For BSkyB there is the extra boost right now from questions bounding around the market over what this cash-generative business will do next. Could it be paying out a hefty dividend or will largest shareholder News Corp decide now is the time to take Sky off public markets and snap up all the shares? Either way, shareholders are setting their sights on a nice windfall and the shares ended up 29p, or 4.9%, at 625p, the second-biggest risers of the day behind InterContinental Hotels, up 6.1% to £11.36 on positive analyst comment.

Analysts had been looking for a strong performance from soap-to-soup maker Unilever as it continues to benefit from expanding emerging markets. In the event the boost was bigger-than-expected and first quarter underlying sales growth accelerated to 4.1%, compared with market forecasts for 3.2% growth.

That left shares in the home of Dove soap and Lipton teas up 64p, or 3.3%%, at £19.80.

Still, the company itself warned the market not to run away with itself, with Dutch-born chief executive Paul Polman flagging up rising commodity prices including for tea, milk and crude oil.

“As they say in Dutch, don’t smoke too much pot, stay realistic,” Polman told investors.

Turning to the fallers, shares in BP tumbled 6.5% to 584.2p as the oil company conceded the Gulf of Mexico oil spill was much worse than first feared.

Moving to the midcaps, housebuilders were in demand after Taylor Wimpey said UK housing market conditions “remain encouraging” and that prices achieved on private homes were up 9% on a year earlier. Still, many shareholders were not happy that management rewarded itself so highly last year, when chief executive Pete Redfern saw his pay package almost double despite the housebuilder reporting a £640m loss. At Thursday’s annual general meeting, 15% of those who voted did not support the remuneration deal. The shares closed up 0.8% at 41.76p.

Finally, further down the market, Raymarine, the debt-laden manufacturer of electronic equipment for leisure boats and perennial takeover target of late, shot up 17.9%, or 2.5p, to 16.25p after it said it “remains in advanced discussions” with a third party regarding a sale.

- BSkyB

- Market forces column

- Unilever

- Whitbread

- Kazakhmys

- AstraZeneca

- Shire

- Taylor Wimpey

- InterContinental Hotels

- BP

FTSE 100 holds gains as Wall St opens higher and Greek fears subside for now

With some solid corporate news from the likes of Unilever in the UK and Santander in Spain, reassurance from the US Federal Reserve on the economic outlook and calmer nerves around Greeces’ woes, the FTSE is on course for relatively strong gains today.

Of course, there could still be a shock before the close - as S&P’s Spain downgrade proved to be yesterday - but for now, with around an hour of trading to go the FTSE 100 is up 22 points, or 0.4%, at 5608. The rise has been bolstered by a stronger open on Wall Street where the Dow Jones Industrial Average is up 78 points, or 0.7%, at 11123.

Markets have been reassured by signs a bailout deal for Greece is nearing and the euro has recovered somewhat from yesterday’s one-year low against the dollar.

In the US, sentiment has been lifted by the Fed’s comments in a statement last night that “economic activity has continued to strengthen and that the labor market is beginning to improve.”

In corporate news, several companies beat expectations today, boosting overall sentiment. Spain-based bank Santander reported a 6% rise in first-quarter profits, ahead of forecasts. In Germany, chemicals company BASF also beat forecasts while Bayer, the chemicals and drugs group, lifted its outlook.

In the UK, media firm BSkyB, consumer goods group Unilever, drugmakers Shire and AstraZeneca, hotels-to-coffee group Whitbread and miner Kazakhmys all beat expectations in their latest updates.

- Unilever

- BSkyB

- Whitbread

- Shire

- AstraZeneca

- Kazakhmys

- Banco Santander

Unilever cheers market with emerging-market driven growth

“Don’t smoke too much pot, stay realistic,” is the warning from Unilever‘s Dutch-botn boss this morning after the home of Dove soap and Lipton teas has sailed to the FTSE 100′s top performers ranks after posting forecast-beating sales.

There had been broad optimism that the consumer goods company could post solid results with analysts last week taking heart from rival Nestle’s upbeat outlook. Today Unilever has outdone those expectations with news of first quarter underlying sales growth accelerating to 4.1%, compared with market forecasts for 3.2% growth. Much of the growth was down to strong trading in emerging markets.

The shares are up 71p, or 3.7%, at £19.87, the highest since March 4. The wider FTSE 100 is up 42 points at 5628 as worries about Greece subside and strong corporate earnings news from around Europe lifts sentiment in equity markets.

Unilever chief executive Paul Polman says in a statement:

“We show strong momentum across all geographies with continued strengthening of our competitive position in line with our strategy. Growth was supported by the quickening pace of innovation and the introduction of brands such as Cif, Domestos, Lifebuoy and Lipton into new markets. Growth has been especially strong in emerging markets despite the heightened competitive activity.”

But looking ahead he is cautious and in a briefing on the latest results he warned of the impact of rising commodity prices, including tea, milk and oil.

“As they say in Dutch, don’t smoke too much pot, stay realistic,” Polman was quoted as saying on Reuters.

In the statement, he elaborates:

“We will face a tougher environment as the year progresses and thus it is more important than ever to stay focused on the consumer. Commodity costs will increase in the second half, economies remain sluggish and competitive intensity will remain high.”

Martin Deboo at Investec re-states a “buy” recommendation with “increased conviction” and comments:

“Unilever have posted what we consider to be a very strong Q1. It represents a material beat to consensus on both growth and margin. In our view, it reflects quality in depth, with simultaneous margin expansion.”

Jeremy Batstone-Carr at Charles Stanley says the results “proved every bit as robust as had been expected.”

Across the Atlantic, there is a similar story from consumer goods company Procter & Gamble, whose profits beat expectations, again boosted by emerging markets.

- Unilever

Taylor Wimpey and upbeat house price survey boost builders

• Double-digit Nationwide house price inflation buoys builders

• Taylor Wimpey says “encouraged” by market improvement

• Its prices achieved up 9%

Housebuilders are in demand this morning after a cautiously optimistic update from Taylor Wimpey and a house price survey suggesting some new life in the market.

Nationwide’s latest monthly snapshot of the housing market showed prices rose by 1% in April, pushing the annual rate of inflation into double figures for the first time since June 2007. The UK’s biggest building society said the average price of a UK property has increased by 10.5% since April last year, and now stands at £167,802.

Also updating the market this morning ahead of its AGM, Taylor Wimpey says it has been meeting management’s expectations in a “gradually improving, but still uncertain, trading environment.”

It comments:

“We are encouraged by the ongoing signs of improvement across our main markets.

“Although economic and political risks remain in the UK, we believe that the underlying shortfall of new build housing and the strong levels of demand will continue to underpin the market. However, we remain concerned that the shortage of consented land will artificially constrain industry volume recovery in the medium term.”

On the UK housing market, it says:

“Market conditions remain encouraging, with continued gradual improvements in mortgage availability and buyer confidence.

“We entered 2010 with a strong order book position and have continued to focus on building on this sales momentum and enhancing margins. We are approximately 99% sold for the half year and 74% sold for the full year targeted completions.”

“Cancellations are running at long-term low levels of 14.8% for the year to date, which is also a significant improvement on the 18.5% in the equivalent period of 2009.”

As for prices achieved on private homes, they are up 9% on a year earlier - of which around 5% results from active changes in mix and approximately 4% from underlying price increases.

The market likes what Taylor Wimpey is telling it and the shares are up almost 3% at 42.59p, among the biggest risers in a FTSE 250 up 29 points, or 0.3%, at 10328. Rival housebuilders are also outperforming the market, with Redrow up 2.6% at 152.4p, Persimmon up 1.2% at 488.1p, Bellway up 1.4% at 772p and Barratt Developments up 1.2% at 128.1p.

- Taylor Wimpey

- Bellway

- Barratt Developments

- Persimmon

- Redrow

HMV disappoints with tumbling winter sales

• UK & Ireland like-for-like sales tumble 13.2% in fourth quarter

• HMV shares down more than 6%

• But company says on track to meet market expectations

HMV has rattled market nerves with disappointing fourth quarter sales this morning. It is blaming the winter weather and tough comparatives but sceptics see deeper problems, with one analyst labelling the shares a “value trap”.

The home of the eponymous film and music stores said its HMV UK & Ireland like-for-like sales tumbled 13.2% in the 16 weeks to April 24.

That “reflects very strong comparatives in this period in the previous two years, reduced levels of campaign activity this year combined with the impact of severe weather at the beginning of the period,” it claimed.

In a trading statement, HMV says that its group like-for-like sales, which includes the embattled Waterstone’s bookselling chain, fell 10.2%. Total sales, which includes a recently acquired chain of live venues, were down 5.8%.

The sales update has overshadowed HMV’s prediction that underlying pre-tax profits will be in line with market expectations of £74.5m. The shares are the steepest fallers on the FTSE 250, down 5.1p, or 6.5%, at 74p.

Turning to Waterstone’s, which had a torrid Christmas ending in the departure of managing director Gerry Johnson, HMV Group reported an “improved trend”, with like-for-like sales down 4.8%.

But some analysts are not so optimistic about any improvements as HMV continues to battle cut-throat competition from supermarkets and online stores as well as changing consumer habits.

Kate Calvert, analyst at Shore Capital, is quoted as saying on Reuters:

“Like-for-like sales decline of 13.2% for the 16 weeks to April 24 is not a pretty number and a massive change on the 1.4% growth reported for the 10 weeks to January 2.”

“We view the shares as a value trap as we do not expect its recent diversifications into live music and ticketing to offset the decline of its core business over the medium term.”

Freddie George at Seymour Pierce is more upbeat and reiterates a “buy” recommendation this morning:

“Encouragingly the company is confident of hitting market expectations for the current year.”

“In respect of sales at HMV, the company will have been impacted by weak revenues in games, a relatively poor pipeline in CDs and DVDs and the inclement weather at the beginning of the period.”

“In 2010/11, the company should benefit from a recovery in game sales, a stronger pipeline in CDs and DVDs, a contribution from the Mama group, which we believe has been under-estimated and a recovery from Waterstones, which appears on track.”

John Stevenson at KBC Peel Hunt is also hopeful the shares will soon be on an upward path:

“Priced to fail, we believe the shares offer upside as new revenue streams kick in.”

- HMV